MV Weekly Market Flash: Risk...

It’s that time of year again. On the cusp of Memorial Day weekend, the shopworn adage reliably rears its head: Sell in May, Go Away? Like most Wall Street folklore this ever-present refrain, a compulsive go-to theme for the financial pundit class, holds a kernel of relevance inside a fog of statistical unreliability. Sure, if you tally up seasonal price trends over the last handful of decades, you will see an average pattern of relative underperformance during summer’s dog days as compared with the rest of the calendar year. Whether the average trend rings true in any given year, however, is little more than a statistical dart throw.

Happy Anniversary

That disclaimer aside, this year it is hard to avoid the looming presence of Sell in May this particular year. We have just passed the one year anniversary of the S&P 500’s all-time high close of 2130 on May 21, 2015. Anyone who sold in May a year ago is unlikely to rue the decision, having managed to avoid a few stomach-churning days last August and a few more in the first weeks of this year while with zero opportunity cost. As noted in recent MVF commentaries, the benchmark index has made a few summit attempts at 2130 but come up short each time. With each failed ascent, investor uncertainty and unease about the market’s future direction increases…or does it?

Postcards from the Valley

One measure of investor sentiment is global equity fund flows, and by that measure investors do appear uncertain. More than $100 billion has flowed out of equity funds since the beginning of the year, with more than $9 billion exiting stock funds in the last week alone. Sell in May, indeed! The sharp V-shaped correction and recovery that spanned the first quarter presumably spooked many. Fears ranging from China’s debt burden to a British exit from the EU, to weak corporate earnings and the weird US political circus remain more or less unabated.

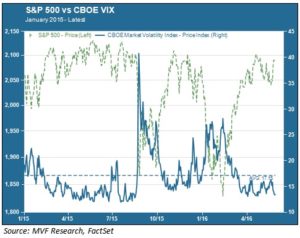

Another common risk benchmark, though, tells a different story. The CBOE VIX index, the market’s so-called “fear gauge,” appears, well, not so fearful at all. Consider the chart below.

The VIX (the solid blue line in the chart) is in one of its low-energy valleys, after being elevated above its long term average for most of the first quarter. Current levels are lower – meaning less risky – than at any time since the first of the two recent stock market corrections hit last August. Of course, the VIX is prone to sudden changes of heart – witness the huge spike last August in the wake of a surprise devaluation of the Chinese renminbi.

Time for a Breakout?

The disconnect between risk as reflected in the VIX and that seen in equity fund outflows may converge one way or the other as a new consensus emerges about the timing of the next Fed rate hike. A spate of recent (unofficial) statements by FOMC members (this commentary is being written before a Janet Yellen speech planned for later this afternoon) suggests that the next move could be coming sooner than markets had earlier anticipated. Could Fed action be the catalyst that moves stock indexes out of their eighteen month sideways pattern – and if so, what is the more likely direction of that breakout?

Predicting near-term market moves is a fool’s errand, but we would caution against leaping to the immediate conclusion that a rate hike in June or (perhaps more likely) July will necessarily send stocks south. Indexes have been firm and largely upbeat with the mercury’s recent rise on the Fed funds futures thermometer. After all, if the move does happen it will reflect increased confidence on the part of the Fed that recent upward trends in wage and price data are more sustainable than they had indicated following the March and April FOMC meetings.

And if it does turn into a bust and markets go south again? Well, we don’t call the floor of that trading corridor a “policy floor” for no reason. The Fed has made it abundantly clear to every woman, man and child in America that it will throw everything it has and more at asset markets to keep them from falling too far. Don’t pin all your hopes on a fast and furious rally – but don’t get overly defensive either. It’s still sound advice to not fight the Fed.