MV Weekly Market Flash: Giving...

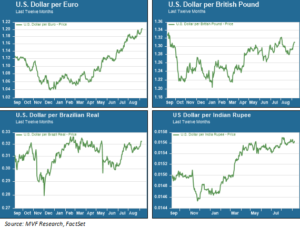

In our commentary last week we made brief mention of the surprising strength of foreign currencies versus the US dollar in the year to date. This week served up yet another helping of greenback weakness, and it is worth a closer look. Perhaps the most intriguing aspect of the dollar’s stumble is how broad based it is, across national economies with very different characteristics. Consider the chart below, which shows the value of two developed market currencies (Eurozone and United Kingdom) and two emerging markets (Brazil and India) versus the dollar.

Brevity of the Trump Trade

As the above chart shows, all four currencies (and just about all others not pictured here) fell sharply against the dollar in the immediate aftermath of the US presidential election last November. Recall that asset markets broadly and quickly coalesced around the notion of a “reflation-infrastructure trade,” premised on the belief that swift implementation of deep tax cuts and a torrent of infrastructure spending would spark inflation in the US and send interest rates sharply higher. Even today, there is no shortage of lazy punditry in the financial media reflexively blurting “Trump trade” every time the stock market turns higher.

But the currency markets long ago signaled the non-existence of the reflation pony in the back yard. In most cases, the foreign currencies’ upward trajectory began late last year or in the first month of 2017. Despite some localized setbacks (e.g. the latest shoe to drop in Brazil’s ongoing political scandal back in May), that upward momentum has continued and gained strength. Even in Great Britain, the negative sentiment surrounding the woeful state of Brexit negotiations has been outweighed by even stronger negative sentiment against the dollar.

Many Stories, One Sentiment

So what is behind this singular sentiment that seems to pervade all continents and economies in various stages of growth or disarray? How long is it likely to last? One of the most popular themes, certainly for much of the summer, has been the perception of stronger growth in the Eurozone. ECB Chair Mario Draghi’s comments on the better than expected growth trend back in late June immediately catalyzed another leg up against the dollar, not just for the euro but for other, seemingly unrelated, currencies. A new consensus set in that the ECB would begin tapering its bond purchases sooner than planned, and Eurozone rates would trend up accordingly.

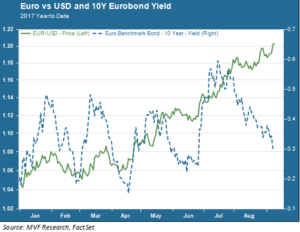

That’s fine as far as it goes, but there would appear to be more to the story. First of all, the Eurozone may be growing slightly faster than expected, but it is hardly going gangbusters. In fact, the real GDP growth rates of the US, Eurozone and Japan are curiously symbiotic. Inflation in all three regions remains well below the 2 percent target of their respective central banks. And then there is the curious case of the euro’s recent strength even while bond yields have once again subsided. The chart below shows the YTD performance of the euro and yields on 10-year benchmark Eurozone bonds.

The spike in intermediate bond yields that followed from Draghi’s June comments has almost completely subsided back to where it was before that. Part of this, we imagine, is due to a more muted ECB posture recently, both at the Jackson Hole summit a couple weeks ago and in comments following the bank’s policy meeting this past week. The falling yields also have to do with a slightly more cautious tone that has crept into risk asset markets as investors take stock of geopolitical disturbances and the disruptive effects of the hurricanes that continue to make headlines in the southern US and Caribbean islands.

None of this would indicate to us that going bearish on the dollar is some kind of “fat pitch” trade, there for the obvious taking. In a world of relatively low growth, the US remains an economic leader in many key sectors from technology to financial services. It would only take a couple readings of higher inflation to bring back expectations for a third rate hike by the Fed and renewed commitment to balance sheet reduction. Recoveries elsewhere in the world are likewise not immune from setbacks that could necessitate a redoubling of stimulus.

That said, national currencies do, to some degree over time, reflect general sentiment towards the prospects of the home nation. Right now, it would be fair to say that those views are mixed, and not necessarily trending in the right direction, as concerns the US. Whether that leads to further dollar weakness or not is by no means certain, but it is increasingly a trend that cannot be ignored.