MV Weekly Market Flash: Bitcoin...

We don’t talk much about bitcoin (or other cryptocurrencies) in this space, mostly because this asset class does not have a place in our asset allocation models. Our advice to clients in this regard is simply: treat cryptos like you would treat any purely speculative wager, be it sports betting or the roulette table in Vegas or whatever else. In other words, a discretionary activity to undertake outside the guardrails of your long-term financial portfolio with specific objectives for growth and capital protection.

Punters Rise, and Fall

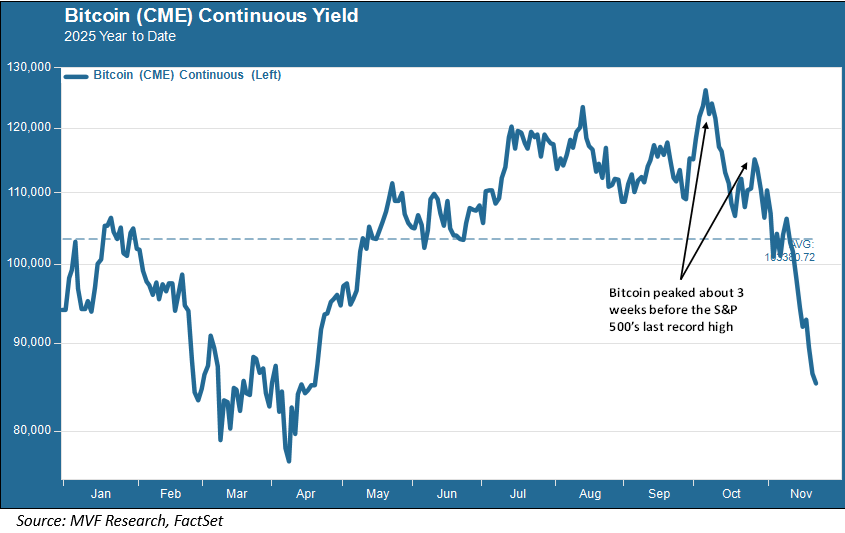

Sometimes, though, a discussion about bitcoin is helpful, and this tends to be the case when it serves as a useful proxy for a market environment that has been awash in speculative fever. As has been the case for much of 2025, ever since traders and other short-term punters dusted off their momentary fears of economic Armageddon in the wake of the April tariff follies. Bitcoin had one heck of a ride, surging by 64 percent from its low on April 8 to a high of $126,315 (per coin) on October 6. But then things went south.

Since that October 6 high, the price of bitcoin has fallen by around 32 percent. Interestingly, bitcoin’s drop started about three weeks before the S&P 500 recorded its last all-time high, on October 28. Needless to say, that 32 percent reversal is far bigger than what the benchmark equity index has experienced – as of today’s market open the S&P 500 was down 5.1 percent from the October 28 high (stocks are trading more or less flat about an hour into today’s session). As we noted in our commentary last week, a number of factors are at play here for equities, including AI bubble concerns, the ongoing data fog problem, evidence of a slowdown in consumer spending and the fragile backdrop of geopolitical instability. Investors have been particularly unwilling to reward strong earnings reports (e.g., yesterday’s Nvidia numbers) while unleashing their full fury on companies that fall short of their expected numbers.

Cash Flows Persevere

In a market environment dominated by speculation and sometimes mindless momentum, it makes sense that the less fulsome assets are the first to fall. For all that Silicon Valley evangelists (and, more recently, late-to-the-party types from Wall Street) have been hyping the importance of cryptocurrencies as a mainstream asset class, they still collectively have yet to demonstrate a convincing use case in the real economy (apart from facilitating shady transactions on the dark web and, well, speculation for its own sake). These assets have no value apart from what people trading them perceive that value to be (this is not true for stablecoins, which is a separate discussion entirely and possibly a subject for a future article). The absence of a convincing real world use case is what keeps cryptocurrencies out of the realm of the asset classes we consider for portfolio construction.

Companies with solid cash flows, manageable debt to equity ratios, and believable models for sales and profits growth, on the other hand, will persevere through the periodic downturns that are an inescapable part of long-term investing. We believe that the most important thing we can tell our clients is to stay disciplined and hold onto their quality assets during the downturns. Trying to guess when to get out is hard; trying to guess when to get back in is even harder and much more likely than not to result in missing out on those important early recovery days after a low point is hit. This discipline is likely to be called on as we head into what could very well be an extremely tricky year ahead.