News & Insights

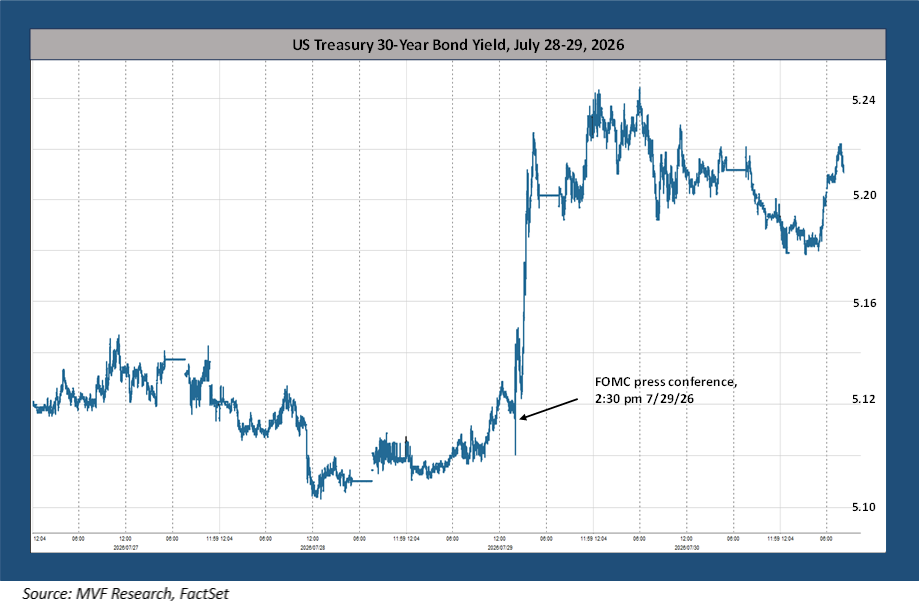

Well, that went over like a lead balloon. Fed chair Kevin Warsh spoke, and the bond vigilantes acted. One tenth of one percent – ten basis points in finance-speak – may not sound like much. But when a staid Treasury bond yield goes up by that much in a matter of minutes, it is a big, big deal. And it is a big, big problem for the new Fed chair as he tries to establish the same level of credibility with the bond market – his most important audience – that his predecessors Powell, Yellen and Bernanke had.

The Substance and the Style

We watched the FOMC press conference as it was happening, starting at 2:30 pm this past Wednesday. To be perfectly honest, we found things with which to agree in the substance of Warsh’s remarks. He noted that the Fed only has direct control over one interest rate – the overnight Fed funds rate – and that market rates elsewhere on the yield curve had been moving up recently amid intensified concerns about inflation catalyzed by the resumption of hostilities in the Midde East. In other words, per Warsh, the market was able to send signals without the customary jawboning of Fed officials telegraphing their intentions – in other words, without the constant forward guidance the Fed has regularly employed since the aftermath of the 2008 financial crisis. The FOMC can then use these clear market signals as part of their deliberations on when to take policy action.

Fair enough – that is a coherent point of view whether one agrees with it or not. But the delivery was lacking. Peppered with questions by the attending journalists about why the Fed was keeping rates on hold in the face of this persistently above-target inflation, Warsh stumbled and gave roundabout answers about “family fights” and “spirited discussions” and the like. That there were indeed elevated tempers during the FOMC’s deliberations was clear from the outcome – three dissenting votes by Committee members who wanted a quarter-percent rate hike. To the bond market, Warsh’s dissembling sounded like someone who might be thinking more about the political consequences of raising rates than the economic rationale for doing so.

Not a Great Time for Confusion

The outcome of Wednesday’s meeting gives the market one more thing to be concerned about, at a time when there are already plenty of things to be pinning onto your wall of worry. Conditions in the stock market appear fragile, with some eye-popping intraday volatility in the hitherto driving force of the AI trade. When established megacap stocks like Microsoft and Meta experience double-digit percentage swings in a single day (one up, one down), it doesn’t scream “stability.” The CAPE (cyclically adjusted price to earnings) ratio of the S&P 500 is just three points below where it was at the peak of the Internet bubble in 2000. The Middle East turmoil is at risk of turning into a forever war. The total amount of US government debt is about to top $40 trillion, with the debt-to-GDP ratio climbing over 120 percent. That’s a number that will have knives out among those bond vigilantes.

In other words, it is not a great time for the market to be confused about the intentions of the Fed. Again, we have no problem in principle with the idea that the market does not need constant spoon-feeding by FOMC members in order to function properly. But that transition needs to be managed carefully. The Fed is the single most important institution for the bond market, and the bond market is the linchpin of the entire financial system. Kevin Warsh, whatever his own personal ideology, needs to be more attentive to the responsibility he holds as the public face of this systemically important institution.