MV Weekly Market Flash: The...

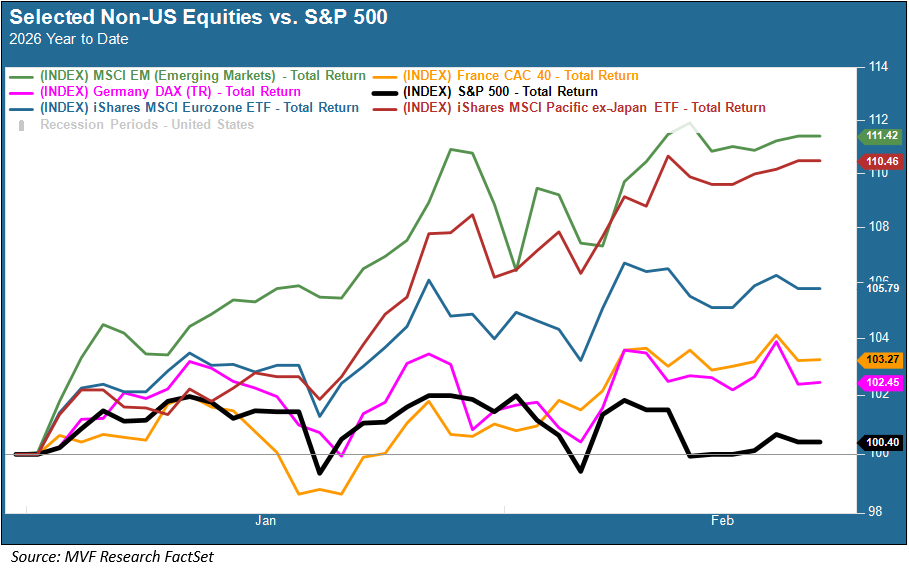

The rotation out of US equities is into its second year and going strong. The rest of the world may be having its share of problems, but underperforming stocks is not one of them. Here is a brief snapshot of how things are going in other parts of the globe, relative to the flattish ways of the S&P 500 thus far.

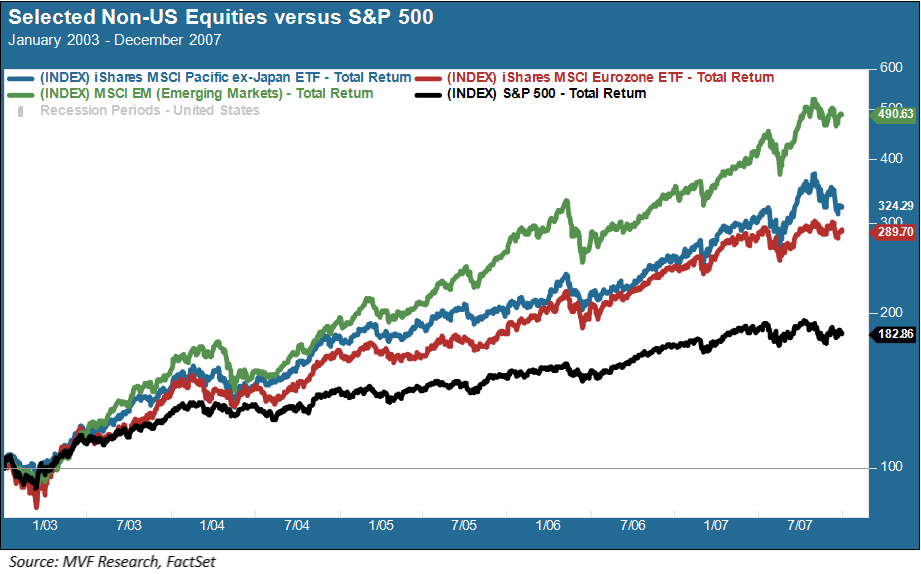

This got us to thinking about the last time non-US equities gripped the imagination and enthusiasm of the investing crowd. Let’s take a little trip back to the quaint world of this century’s first decade.

Swan Song for the Global Age

In hindsight, we know that it was the last gasp of the Global Age – the final five years of the quarter century in which the neoliberal trinity of open borders, light-touch regulation and unconstrained capital reigned as the unapologetic Zeitgeist. But for those of us living in those years, sandwiched in between the dot-com crash and the global financial crisis, 2003 to 2007 was just another chapter in the “end of history,” briefly interrupted from late-1990s good vibes by said bursting of the tech bubble, but with the Clinton-era directive to not stop thinking about tomorrow still circulating endlessly in our limbic regions.

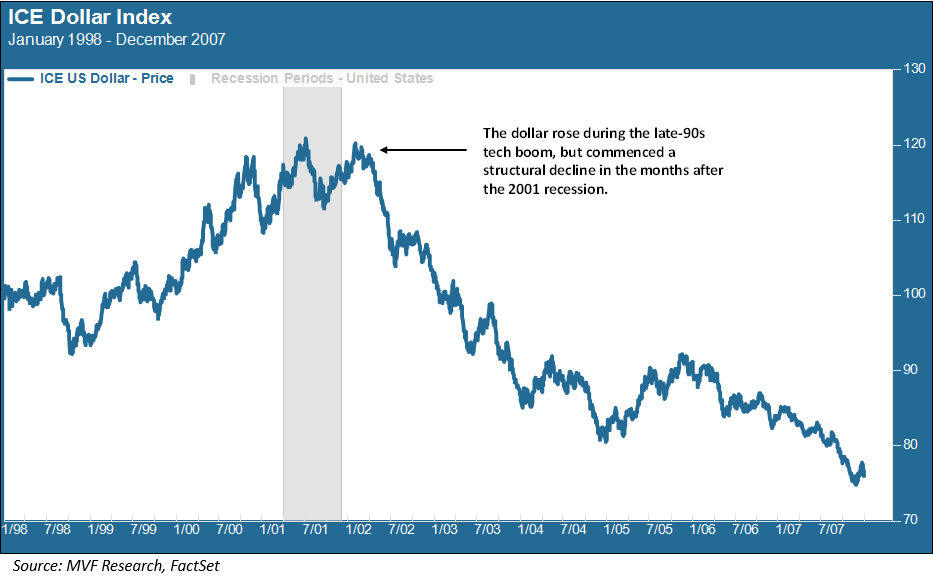

The US dollar, which had risen steadily during the world’s love affair with everything dot-com, held its own during the 2001 recession, but started to falter the following year, setting the stage for what would become the great non-US equity rally of the mid-aughts.

What caused the decline of the dollar and the related move out of dollar-denominated assets? Several variables were probably at play, including the simple fact that the late-90s tech boom was almost entirely a US affair, so a “sell America” impulse was natural when that play fell out of favor. But there was more to it than that. The outperformance by international equities of almost every stripe over their US counterparts was solid, structural and sustained over this entire five-year period.

This was the period when China’s fast-growing economy blasted into its supercycle phase. Observers suddenly realized that all those jobs which had left the US due to offshoring in the 1980s and 1990s were not reappearing all over the world as hubs in an increasingly complex global supply chain. The word of the day was “decoupling,” as in the growing independence of these emerging regional clusters without the need for depending on capricious portfolio investment from Western capitals. The non-US world, and especially the emerging parts of that world, were destined to grow faster than the established West. Faster growth would mean more prosperity and, sooner or later, companies that would be every bit as good as, if not better than, their Western counterparts.

Decoupling Arrives, Twenty Years Later

Things didn’t work out that way, as we now know. The global financial crisis knocked all stock markets for a nasty loop, and the Great Recession set in. The Eurozone nearly fell apart in the early 2010s. China’s supercycle ran out of steam in the middle of that decade, prompting a major devaluation of its currency and a collapse in Chinese equities. Meanwhile central banks, led by the US Fed, took over the job of rebuilding the economy by providing ultra-cheap money. That easy money, in turn, catalyzed animal spirits in Silicon Valley to invest in audacious tech projects, some of which became extremely successful. US assets were back in favor, led by the tech giants and some of the smaller pilot fish that swam along in their wake.

Finally, though, the decoupling moment that had been imagined back in the mid-2000s arrived, last year. The old Washington Consensus of a global village unified under the neoliberal banner of free trade, judiciously overseen by the US, is gone. China is ascendant, Europe is regrouping into a post-Pax Americana order, and even Japan is showing some moxie again as the country rallies to its new and extremely popular prime minister. What all of this is going to look like five years from now is anybody’s guess. But the composition of global asset markets is likely, we think, to be quite a bit more diversified than it is today.