News & Insights

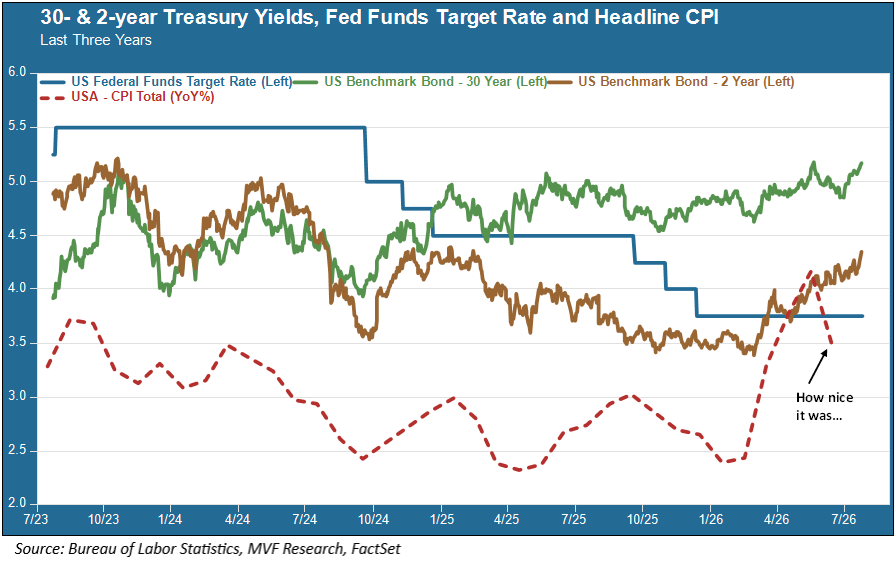

How quickly it all goes away, like the snows of yesteryear. Just last week, the Bureau of Labor Statistics delivered a cheery inflation report showing that the headline Consumer Price Index had actually fallen – yes, gone down and not up – for the month of June. That pleasant reversal was largely due, of course, to falling energy prices as tempers in the Middle East seemed to be cooling off. Gas prices were coming down just as the summer travel season was ramping up, a nice change from the usual. Maybe it was even time for a rethink on the likelihood of a Fed rate hike later this year.

And then it all went south again. We won’t see the July CPI report for a few weeks, but in the meantime we do know what oil prices are doing in the wake of the Middle East war returning to its hot phase. And interest rates are sending their own very clear message.

Another Strait Heard From

Brent crude oil popped back over $100 per barrel on Thursday and remains in a narrow range on either side of that level today. Thursday also brought another memorization exercise for geography-challenged Americans in the form of the Bab al-Mandab Strait, a narrow body of water off the western coast of Saudi Arabia, through which tankers carrying oil from Red Sea ports like Yanbu and Jeddah must pass in order to get to the Gulf of Aden and onto their export markets in the Indian Ocean and beyond. Two such tankers were struck there by Houthi militants, a Yemeni-based group supported by Iran. So not only is the war back on, but its geographic footprint is expanding. The Houthis have claimed their intention to force closure of the strait in the same way that the Strait of Hormuz, on the other side of the Arabian Peninsula, has complicated passage for the past three-plus months.

As of today (Friday), the situation remains unclear. The US has threatened a massive retaliation in response to the Houthi action and ongoing attacks throughout the region by Iran itself, but whether that translates into action or merely another round of idle bluster is unknown. Some targeted US strikes took place earlier today after the apparent rejection by Iran of a peace deal delivered by the president of Iraq, acting as an intermediary. Markets appear to be mostly in a waiting mode, with not much happening so far today in commodities, interest rates or the stock market.

Tariffs Again, Really?

Amid all of this, it seems slightly surreal that the US administration is apparently pushing ahead with another batch of tariffs, but here we are. This new round of tariffs appear to be an attempt to legitimize the implementation of duties on imports following the Supreme Court’s rejection earlier this year of most of the tariffs implemented last year under the International Emergency Economic Powers Act. The current proposed tariffs, which range from 10 to 12.5 percent and the adverse effects of which appear mostly directed at Asian and Latin American exporters, flow from Section 301 of the 1974 Trade Act.

But wait, there’s more! In addition to those blanket Section 301 tariffs, the administration has delved into an even more bizarre provision – this one from the infamous Smoot-Hawley Trade Act of 1930 – to throw a bunch of duties amounting to 50 percent on specific goods from our eternally patient neighbor to the north, Canada. The Smoot-Hawley Act, as students of economic history know, was a key factor in the malaise that became the Great Depression. Reviving that misbegotten lump of trade policy from the 1930s seems particularly inadvisable amid everything else that is going on today.

The Fed will meet next week, and while the most likely outcome of Wednesday’s policy meeting will be to hold rates steady, this will be what observers call a “live” meeting with the potential for surprises. At the very least, it may suggest what lies in store when the Committee meets again in September, which will be a Summary Economic Projections event and will have access to another two months’ worth of inflation data beyond what we know today. This could be one of those September-October periods with more tricks than treats.