MV Weekly Market Flash: A...

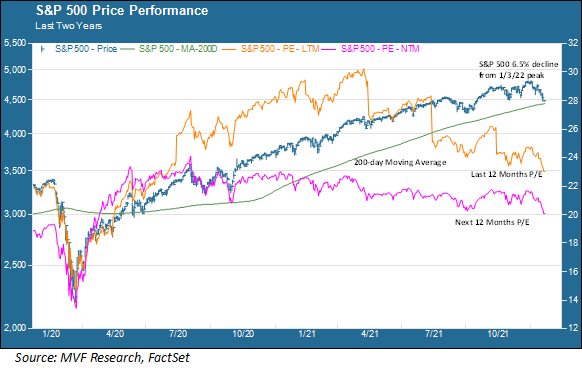

It has been quite an opening act for the year ahead. On occasions like this we always find that a little perspective can be helpful. With that in mind, let’s consider the price performance for the S&P 500 in the first three weeks of 2022 in the context of the past two years.

We’ll see today and in the days ahead whether the 200-day moving average, a technical indicator that has no inherent substance but does tend to function as a support level for short-term trading strategies, signals enough of a buy-the-dip opportunity to reverse some of the recent weakness. At least as of now the pullback in equities is not particularly unusual (it’s also worth noting that the next twelve months P/E ratio is currently as low as it has been any time since the pandemic lockdown period in March-April 2020). In terms of going forward, a great deal will depend on how the market reacts to a number of key pieces of information on tap for next week.

Setting the Table for March

First up of note next week is the Fed. The Federal Open Market Committee meets on Tuesday and Wednesday, with the usual press conference to follow after the Wednesday meeting. The FOMC is always followed closely, but this time even more so than usual as investors are expecting guidance on the calendar for raising interest rates. All signs point to at least three, and possibly more, rate hikes in 2022 given the Fed’s recent strong stance on fighting inflation as job number one (as we discussed in detail in last week’s commentary). One bit of chatter currently making the rounds in financial circles is that at the March FOMC meeting the Fed will do a “twofer” and raise the Fed funds target by 0.5 percent rather than the more customary 0.25 percent increment. Jay Powell is unlikely to tip his hand that clearly next Wednesday. But if he pushes back hard against 50 basis points in March, the market may interpret that as a relatively dovish signal, which in turn could lend some support to stocks.

Reminder, We’re Still Growing

On Thursday next week we get the first look at Q4 GDP, which economists are predicting will show year-on-year growth of 5.2 percent. Assuming the actual number comes in somewhere around the estimate (never a sure thing) that may also be a positive sign. With all the focus on inflation, it is easy to forget that the economy is still growing, with no meaningful signs of a recession on the horizon. It is the rare market pullback that turns into a sustained bear market in the absence of an economic recession (Black Monday of 1987 being the only recent exception, and even that was relatively short-lived).

The GDP number will come in the middle of a thick batch of earnings reports, with tech heavyweights Microsoft and Apple among the many companies that will be issuing Q4 reports next week. So far in this still-young earnings season the glass seems to be more half-empty than half-full, with analysts expressing disappointment over forward guidance (see for example Netflix’s guidance on Q1 new subscribers at 2.5 million compared to Street expectations of 4 million) and concerns about inflation’s effect on profit margins. Nonetheless, overall Q4 earnings growth is still expected to come in around 20 percent, and the outlook for 2022 earnings remains in the range of mid-high single digits.

Another Look at Inflation

That brings us to Friday, when the Personal Consumption Expenditures (PCE) index, the Fed’s preferred measure of inflation, comes out. The consensus forecast has headline PCE registering 5.7 percent and the core (ex food and energy) showing 4.8 percent. This is the one nobody wants to see coming in way ahead of expectations. Treasury Secretary Janet Yellen recently opined that, in the event of the pandemic finally getting under control once the omicron wave peaks, she would expect to see inflation back down around two percent by the end of this year. That would be welcome news, but it will very much depend on the Fed’s ability to demonstrate credibility in sufficiently fighting off more endemic inflation through monetary tightening (while at the same time not choking off growth and hastening a recession).

So there is a lot at stake next week. In the meantime, we might advise taking another look at that 2-year S&P 500 chart above and tuning out the predictable cacophony in the financial media with their red flashing arrows and hyperventilating anchors. Pullbacks happen. Discipline, patience and rational thinking get us through them.