MV Weekly Market Flash: A...

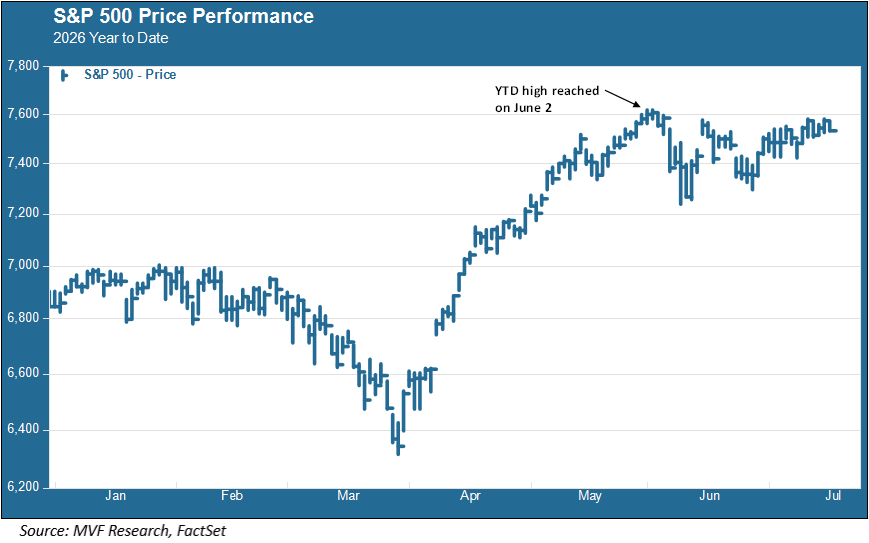

It has been seven weeks since the S&P 500 reached its most recent year-to-date high, closing on June 2 with a 16.9 percent total return. Since then, US stocks have mostly meandered along a sideways pattern in the aggregate, but with some very wide spreads between intraday highs and lows. As we head into the typically slow summer doldrums, when light volume can exacerbate movements for any old reason, it’s worth pondering whether what’s going on is just technical positioning based on things happening now, like traders going through the mechanics of adjusting to SpaceX’s arrival on major indexes, or more worrying signs of a major rethink in longer-term outlook.

Lots of Moving Parts

The first meaningful catalyst to pull the market back from its seemingly easy glide up during April and May had nothing to do with SpaceX at all, but rather the monthly BLS jobs report that came out on June 5. That report showed nonfarm payrolls rising by 172,000, well above what economists had predicted. A hot jobs report, while presumably good for participants in the labor market, is not great for anyone (like a bond trader) concerned about the prospect of rising interest rates. The Federal Open Market Committee would be meeting shortly to discuss interest rates, and this jobs report looked set to nudge the thinking in the Eccles Building closer to a consensus around raising rates.

Some of what happened between the June 5 jobs report and the June 17 FOMC meeting (at which rates were held at present levels but with a hawkish tilt) can most likely be ascribed to short-term mechanical tinkering. SpaceX did indeed go public on June 12, amid breathless hype from the top-tier Wall Street firms underwriting the bonanza and passive index managers figuring out how to reallocate their holdings to accommodate the noisy new member. But over in South Korea the KOSPI index, which had become a central player in the latest chapter of the AI story with its concentration of memory chipmakers, started doing some very wild gyrations as investors started to connect the dots between the surging prices of these in-demand memory chips and the more general problem of inflation across all parts of the economy. The heightened volatility on the KOSPI made itself felt in AI spaces elsewhere in the world. After the market close on June 24 Micron, a US-based memory chipmaker, published a blockbuster earnings report showing that the greater part of a 345 percent increase in sales came from higher chip prices. The next morning, Apple announced that it would be raising prices on certain Mac books and iPads in large part due to higher cost pressures from memory chips.

Re-running the Numbers

All this has added to what was already a much more complex set of interwoven threads than the simple moniker “AI narrative” would suggest. These companies – chipmakers of various types of semiconductors, hyperscalers, power suppliers, frontier model platforms and everyone else in the AI ecosystem – interact with each other in a variety of ways as buyer, seller, investor, partner, advisor and a whole lot more. Following the money in this labyrinthine world is no easy feat. And while it does not appear that the market is visibly souring on the economic importance of AI, with few if any signs of demand abating for compute, for data center investment or for the scientific talent to run the models, this stock market pause suggests that some rethinking and repricing is going on.

For the time being, at least, conditions seem top-heavy. Not for the first time or even the sixth time since AI mania got into gear in early 2023. But the market is also not at 2023 valuation levels. The S&P 500’s CAPE (Cyclically Adjusted Price to Earnings) ratio was a bit over 41 when the index registered that June 2 year-to-date high. That is only three points lower than where the CAPE was in March 2000, at the zenith of the dot-com bubble. That is not to say that the market is due for a March 2000-style fall. But it does weigh in on what is going to happen when this sideways pause gives way to another directional trend.

Eventually, the summer dog days will give way to the historically tricky period of the transition from third quarter to fourth quarter. September and October contain a treasure trove of spooky stories from years past for spicing up evenings around the campfire. This might be a good time for a re-examination of prior assumptions and alternative scenarios.