MV Weekly Market Flash: A...

The collapse in oil prices was arguably the headline economic story of 2014. The malaise carried into January of this year, with prices of key benchmark crudes hitting six year lows last month. A sharp rebound in the first two weeks of this month has observers wondering if the slide is over, and, if so, what that may portend for the months ahead. One interesting development, which will be the focus of this post, is a significant widening of the spread between two of the most widely-referenced benchmarks: Brent crude and West Texas Intermediate crude. Why is this seemingly arcane byway of commodities markets of interest? In our opinion it sheds light on some key supply and demand factors at play that may influence economic and asset market trends as the year winds on.

Crude Realities

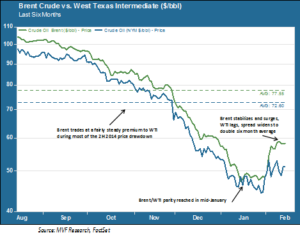

We normally think of commodities as fungible – one person’s barrel of oil or bushel of wheat is the same as the next person’s. While that is true in the abstract, the reality is that the prices of many commodities are strongly influenced by differentiating factors. Crude oil is a case in point. There are many “flavors” of crude oil, measured chiefly by a range of densities (light to heavy) and sulfur content (sweet to sour). These determine how a given barrel of crude is used – for gasoline, jet fuel, home heating oil etc. The location of crude oil sources also matters. Brent crude, a light-sweet variety, comes from the North Sea between Great Britain and western Scandinavia. West Texas Intermediate is also a light-sweet variety, but as the name would suggest it is produced and traded in the U.S. mid-southwest. The chart below shows the price trends for both benchmarks over the past six months.

Brent and WTI crude are quite similar in terms of density and sulfur content, and so all else being equal one would expect them to trade at or close to the same price. All else is not equal, of course. As the above chart shows, Brent crude has traded at a premium to WTI for almost all of the past six months, and in fact the Brent premium has been a staple feature of the market for a much longer period. However, Brent prices plunged at a faster rate in the final throes of the price meltdown, reaching parity with WTI in the middle of last month. It was a brief parity. In the second half of January Brent oil stabilized while WTI continued to fall to new lows. The percentage spread between the two benchmarks is now more than twice its last six months’ average. A barrel of Brent crude is more than 6% dearer today than on January 1, while WTI crude is about flat year to date. What’s behind this divergence?

Texas Hold ‘Em

Both supply and demand are at play here, but the trend of U.S. oil prices is at heart a supply story. We are producing more oil, at a faster rate, than at any time since the early 1980s. Financial media chatter to the contrary, the pace does not appear to be slacking off despite the global plunge in prices. Last week both crude oil production and inventories reached record levels. And domestic oil production is a captive of home-grown demand; the export of U.S. crude to other markets is prohibited by current government policy. Whatever is left over in the storage tanks after U.S. orders have been filled stays in the tanks. Energy-hungry manufacturing economies in Asia and elsewhere get their stuff from other sources, including the North Sea.

A number of the major exploration & production (E&P) companies have announced plans to delay forthcoming U.S. drilling projects, and that may help provide more price support down the road. And there is a reasonable possibility that the export ban may weaken or be eliminated in the not too distant future, which would open new sources of demand. But the supply-demand imbalance shows few signs of going away any time soon. If indeed prices have found a structural floor, they may still face significant headwinds in getting anywhere close to the $100-plus levels where it has traded for most of the past five years. Which may not be a bad thing at all; “stable and low” may turn out to be a pretty nice recipe for consumers, businesses and stocks alike.