MV Weekly Market Flash: Big...

Black Tuesday, 1929 turned out to be a big deal. Black Monday, 1987 – not so much. The history books all duly note that the Wall Street crash of October 29, 1929 marked the opening act of the Great Depression, during which the US stock market at one point in the early 1930s had lost 80 percent of its value from the 1929 peak. The market did not recoup all its losses from that ’29 high point until 1954.

Conversely the 1987 crash, dramatic as it was on that one single day on October 19, did not usher in anything other than a few weeks of higher-than-average volatility before the growth cycle of the mid-late 1980s resumed in full. Though in all fairness we should note that Black Monday ’87 did spawn a fairly well-received TV series on Showtime, a feat that so far has eluded the Crash of ’29.

With this in mind, folks paying attention to the market chatter this week may have heard the phrase “Black Wednesday” pass the lips of pundits who study the fossil fuels industry. To be perfectly honest, we are of the opinion that this trope of “Black X-day” itself, so beloved of Wall Street bards, is dated, stale and overdue for retirement. But we do agree that what happened this past Wednesday was significant enough that the day may wind up being one of those rare turning points identified by future historians.

Calling Engine No 1

So what happened on Wednesday? Within roughly a 24-hour period three major things took place in the world of Big Oil. At the annual shareholder meeting of ExxonMobil, the oil behemoth ceded at least two seats on its board of directors to a climate activist group called Engine No 1 (the group is expected to gain a third seat when the official vote count is completed sometime next week). To put it mildly, ExxonMobil’s management is not used to contested shareholder votes like this, particularly when the start-up activist group (Engine No 1 was founded just last year) was backed by some of the company’s largest institutional investors including BlackRock and Vanguard. The activist board members plan to be vocal in putting pressure on ExxonMobil to sharply reduce its oil output.

Something similar happened to Chevron at its general meeting on the same day: shareholders voted on a measure to set strict emissions targets from the products it sells. And while green-minded shareholders were finding their institutional voice here in the US, a perhaps even more far-reaching decision was handed down across the Atlantic. A Dutch court in The Hague, Netherlands, ruled that Royal Dutch Shell must reduce its carbon emissions by 45 percent by 2030 against its 2019 levels – on an absolute basis, which is stricter than the carbon intensity targets (amount of carbon per megajoule of energy sold) that the company prefers to use as its benchmarks. That’s not a suggestion – it’s a demand backed by law.

What’s the Market Impact?

Wednesday’s events didn’t reverberate in any kind of immediate panic selling by investors of energy shares. There was a bit of a midweek dip in Big Oil, but prices quickly stabilized. Indeed, the overall narrative for the energy sector so far in 2021 has been mostly positive. Fears of higher inflation, coupled with expectations of surging demand and supply shortages in key goods, have drawn investors to real assets like industrial and energy commodities. Energy is outperforming all other major S&P 500 industrial sectors in the year to date.

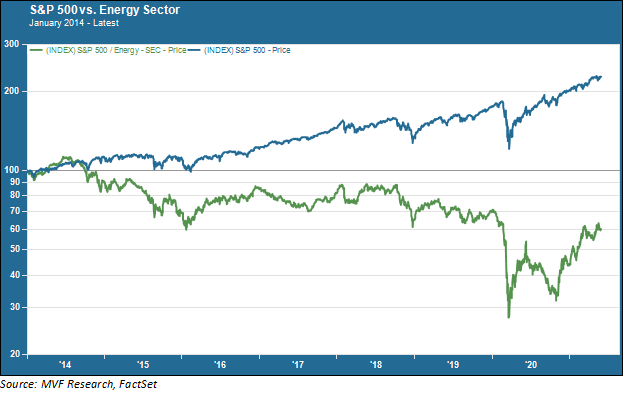

The sense among those who closely follow the energy industry is that the tangible effects of Wednesday will take some time to materialize, and in the meantime they are not quite ready to quit the sector while those positive short-term dynamics are still in play. But “short term” is the operative phrase here. In a bigger-picture sense one could argue that the market has already rendered its verdict on the future of Big Oil, well ahead of what happened this past Wednesday. The chart below shows the performance of the energy sector against the S&P 500 from the beginning of 2014 to the present.

Even with the sharp rally in energy shares that started late last year, the sector is worth only 60 percent of its value at the beginning of 2014, while the benchmark index has more than doubled in value. The longer-term question for the diversified energy majors like ExxonMobil and Royal Dutch Shell is whether this new level of direct pressure – from shareholders, from the courts and from general public opinion – will push them to more aggressively develop core competencies in clean energy sectors.

They will certainly face challenges if that is the route they choose – from agile clean energy companies already staking out real estate in the emergent sector to their own stale institutional cultures based on more than a century of assumptions about the primary role of fossil fuels in the economy. It’s not impossible. But at this juncture it would seem like a long shot. Wednesday May 26 could potentially be one of those narrative markers that actually stands the test of time.