MV Weekly Market Flash: Big...

Well, it’s the last day of October (Happy Halloween!), and unless something really freaky and ghoulish happens between now and 4:00 pm today Eastern daylight time (don’t forget to turn the clocks back on Sunday), we will have managed yet again to avoid an October Scare, that creepy phantasm given to showing up every now and then in years otherwise unconnected – 1929, 1987, 2008 to name a few – with a bag full of tricks and no treats. This year, despite the inescapable return of bubble banter among the financial chattering class, the S&P 500 has added 2.3 percent to its year to date price performance since the end of September.

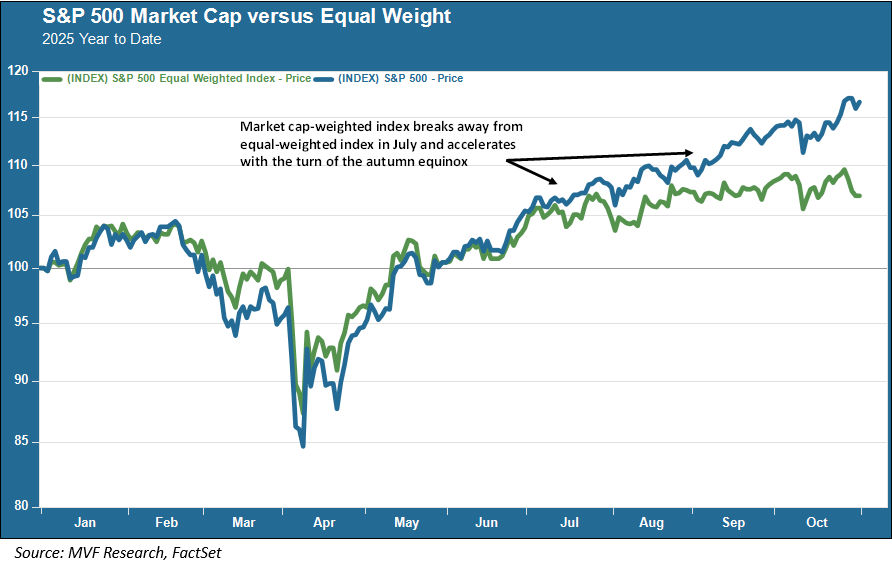

Second Half Surge

In fact, much of the market’s giddiness in recent weeks has happened in that very same segment of mega cap AI-themed stocks that has generated the lion’s share of the bubble chatter. It was not always thus. For the first half of the year, the so-called Magnificent Seven and its posse of AI fellow travelers didn’t stand out in any meaningful way from the rest of the market. The chart below shows the year to date relative performance of the S&P 500 benchmark index, which is weighted by market capitalization and thus influenced in an outsize manner by the movements of the largest companies, and the S&P 500 equal weighted index (which, as the name suggests, takes away the influence of the market cap factor).

The acceleration of the Big Tech-concentrated second-half surge was on prominent view this week. On Tuesday, the S&P 500 finished in positive territory largely thanks to just two names – Nvidia and Microsoft – while 75 percent of the companies in the index finished lower on the day, as did eight of the 11 main industry sectors. On Thursday, shares of Alphabet (Google’s parent company) jumped three percent even while the index itself lost nearly one percent as investors responded to a more hawkish than expected report from the Federal Open Market Committee the day before. This morning (Friday), Amazon is up nearly 12 percent on the day following a blockbuster earnings report delivered after yesterday’s market close. Amazon’s strength, which has little to do with Prime shipments of Halloween tchotchkes and lots to do with robust demand for AI and cloud services from its AWS business segment, seems to be giving the AI optimist crowd an argument against the many recent concerns expressed about the apparent circularity of the AI ecosystem.

The End Is Nigh…Near…Never…

It’s one thing to observe a bubble and proclaim its existence; it’s another thing entirely to predict how much longer the animal spirits have to run. After all, Alan Greenspan made his “irrational exuberance” comments about the building tech bubble in 1996, several years before the thing finally imploded in March 2000. The AI infrastructure bonanza does not appear to be on track to end any time soon. Among the tidbits to take away from this week’s earnings reports was the tidy sum of $80 billion in capital expenditures on AI-related items by just three companies – Microsoft, Alphabet and Meta – with much more than that promised for the year ahead. The build-out of data centers to power the large language models for AI software is increasingly a must-have component for GDP growth. According to a recent analysis by Harvard economist Jason Furman, investment in data centers and information processing technology accounted for virtually all the GDP growth for the first half of this year. As long as this multibillion dollar spending frenzy occurs, it seems, the economy has a pretty solid cushion against falling into negative growth. Of course, when and if all this spending turns into real productivity across the economy is the question that will keep us all guessing for the foreseeable future.

Meanwhile, the bubble talk won’t be fading away any time soon. Keep an eye on that relative performance trend between the market cap and equal cap indexes, which is likely to look quite different on the other side of a bursting bubble.