MV Weekly Market Flash: Bonds...

It doesn’t take much these days. “Pretty bad market today, huh?!” came one comment from a fellow runner during a muggy 5K outing on Thursday evening. Was it? Apparently so. Thursday’s S&P 500 posting of minus 0.82 percent was the biggest daily drawdown since the second half of June, when the index shed close to 3 percent for some vague reason long forgotten. None of this in any reasonable way qualifies as a pullback of note – we tend not to raise an eyebrow until the 5 percent threshold approaches. But after three months during which the market climbed as relentlessly as the humidity index in the Washington DC swamplands, even a modest pullback of less than 1 percent seems as rare as actual fall weather in this weirdest of October climes. Blame it on the bonds.

Goodbye, Inversion

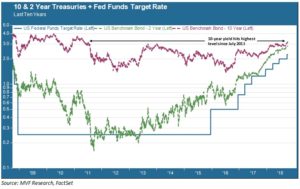

The catalyst for the Thursday downdraft in equities was a surge in bond yields that gained steam on the back of a couple economic reports on Wednesday – in particular, a thing called the ISM Non-Manufacturing Index, which rose more than the consensus outlook. That report, suggesting that activity in the services sector (which accounts for the lion’s share of total GDP) was heating up, set the stage for expectations about a gangbusters monthly jobs report on Friday. The 10-year Treasury yield shot up by 10 basis points (0.1 percent), which is huge for a single day movement. The 10-year yield is now at its highest level since 2011, as shown in the chart below.

That blockbuster jobs report, as it turned out, never happened. We got a headline unemployment rate of 3.7 percent that is the lowest since – kid you not – 1969, that groovy year of moon landings and Woodstock. But payroll gains, the most closely watched indicator, rose by considerably less than the expected 185K while wage growth came in right at expectations with a 2.8 percent gain. Overall, a mixed bag. Equities are roughly flat in tentative trading as we write this, while the 10-year Treasury yield continues its advance. The yield spread between 10-year and 2-year Treasuries, which earlier this year appeared on the tipping point of an inversion (in the past a reliable signal of an approaching recession), has widened to about 35 basis points.

This widening spread would be consistent with the ideas we communicated in last week’s commentary about increased inflationary expectations on the back of an ever-tightening labor market and price creep from higher tariffs on an expanded array of consumer products. So far the numbers – in particular today’s jobs data and last week’s Personal Consumption Expenditures (PCE) reading – don’t bear out the hard evidence. But the bond market could be adjusting its expectations accordingly.

Doing It On the QT

Or, maybe not. There were a couple technical factors at play this week as well, including a jump in the cost of hedging dollar exposure which had the effect of reducing demand for US Treasuries by foreign investors. This is not the first time that we have seen a sudden back-up in yields, only to dissipate in relatively short order. As for the fabled bond bull market that has endured since the early 1980s, well, there is certainly no shortage of times this has been pronounced dead, only to rise again and again.

Ultimately, of course, it all comes down to supply and demand. We know one thing with confidence – the Fed is out of the market as a buyer. While last week’s FOMC meeting didn’t produce much in the way of surprises, it did codify the understanding that the age of QT – quantitative tightening – is at hand. The Fed’s assessment of the economy is quite upbeat. The cadence of rate increases and balance sheet reduction is likely to continue well into 2019.

None of which necessarily suggests that intermediate and long term rates will surge into the stratosphere. If the domestic economy stays healthy then domestic assets should be attractive to non-US investors – an important source of demand that could keep yields in check. Indicators like corporate sales (growing at a brisk 8 percent or so) and sentiment among businesses and consumers (leading to increased spending and business investment) suggest that there is more to the current state of the economy than a fiscal sugar high from last December’s tax cuts. For the near term, our sense is that the positives continue to largely outweigh the potential negative X-factors. We may be okay in 2019 – but 2020 could be an entirely different story.