MV Weekly Market Flash: De-Mystifying...

A great deal has changed in the world of finance since both of us got into the industry way back in the 1980s. One thing has not changed. Practitioners of the financial arts seem to love nothing more than taking a simple idea and making it sound as densely complicated as possible. No wonder so many people are intimidated by finance. They shouldn’t be!

Finance is a bit like knitting: it looks more complicated than it really is. The most elaborate Scandinavian-pattern sweater boils down to just two things: the knit stitch and the purl stitch. Likewise, the most incomprehensible-sounding hedge fund strategy is ultimately about nothing more than the timing, magnitude and level of uncertainty around a series of future cash flows. Once you get the basics down, the rest is relatively easy. That’s the little secret the industry desperately wants you not to know.

Smart Beta, Dumb Marketing

So let’s take a look at one of the popular buzzwords in today’s markets: factor investing. What does that mean? It sure sounds impressive. You might hear a sales pitch in which the smooth-talking industry maven casually intertwines “factor investing” with another beloved piece of gobbledygook: “smart beta.” Wow, a Greek letter and everything! You’ll hear how this is the way the pros invest now, you’ll hear the words “quantitative” and “algorithm” repeated over and over again, and the amygdala section of your brain might light up with residual fears of the binomial theorem you hated so much in eighth grade algebra.

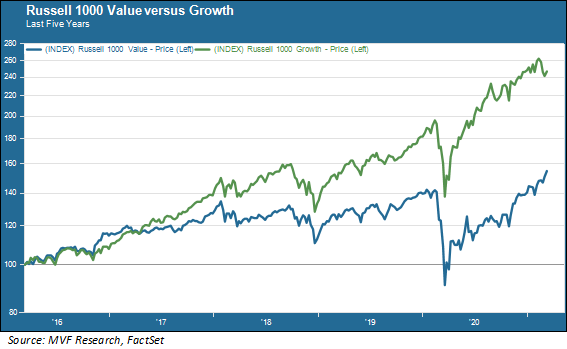

We’re going to show you a picture of what a factor strategy looks like in the chart below, so as to de-mystify all the silliness. We’ve chosen two factors with which you are probably familiar: value and growth.

A Factor Is Just a Point of View

Yes, value and growth, those old standbys of asset class diversification, are factors! You might know them as “styles,” because that’s what they were before they became “factors.” It’s just a new word for an old concept. Style investing became popular in the 1990s, following the academic research of folks like Eugene Fama and Kenneth French in the early years of that decade. In fact, Fama and French came up with a model that discovered (based on long-term data they studied from over the three previous decades) a sustainable advantage to investing in small cap versus large cap, and in value versus growth. Hence the Fama-French Three Factor Model – yes, they called them “factors” but the fashionable investment strategies that proceeded from their research in that decade preferred the term “style.”

Until now, when the fusty old academic term became retro-chic. Meet the new boss, same as the old boss. A factor, or a style, or whatever else you want to pull out of Roget’s Thesaurus, is just a point of view. And not necessarily one that lasts. Consider that chart above. The factor that has shown its dominance over this recent five-year period wasn’t Eugene Fama’s value effect at all: quite the opposite.

So What About that Smart Beta Thing?

But wait, you might say, what about that other phrase, the one with the intimidating Greek letter? Yes, the financial industry does love its Greek alphabet, from alpha to omega. “Smart beta” is just another way to say factor, or style, or point of view, or any other phrase easily constructed with the twenty-six letters of our own alphabet. In case it ever comes up, though, here is the etymology.

So first of all, plain old beta is simply a measure of relative risk. Take a broad market index, like the S&P 500 or the Russell 3000, and assign it a beta of 1.0. Then you measure the variance of a single asset – could be a single common stock, or an ETF representing an industry sector, or a mutual fund – against the benchmark. If the asset varies by more than the benchmark it will have a beta greater than 1.0 – in other words, more risky. Less variance means a lower beta. So good old fashioned beta means investing according to whether you want to assume more risk than the market, or less risk.

“Smart” beta really is not smart at all. Just different – again, a different factor, a different point of view. Do you think that stocks which have recently outperformed the market will keep on outperforming? Then you may choose momentum as your factor. Or you may think the wheel is going to turn and the “dogs of the Dow” are due for their day in the sun. Or you may get technical and cull out stocks which exceed a certain financial threshold: say, the stocks in the S&P 500 in the top 10 percent according to return on equity, or cash flow return on invested capital, or the lowest level of net debt to total equity. Or a mix of all of the above.

Factor outperformance comes and goes. Even the most durable – like the small cap and value factors Fama and French detected back in the early 1990s – are vulnerable to the tectonic shifts that happen in markets over long time periods. The more ephemeral ones can pop into and out of favor within much shorter time frames. Many of them rely on adroit market timing, and market timing is a fool’s errand.

None of which is to say that factor investing is a bad idea. Different points of view should, if done properly, add to a portfolio’s diversification, which is s a good thing. But there is nothing mysterious about factor investing either. Knit one, purl one. Cash flows matter, and the rest is just conversation.