MV Weekly Market Flash: Emerging...

If you parked a chunk of cash in emerging markets equities at the beginning of this year, you are probably giving yourself a pat on the back for your keen investment acumen. While the S&P 500 struggles on either side of break-even for the year to date, the MSCI Emerging Markets index is up a brisk 8% for the same period. And since most broader EM indexes are still well below their recent and all-time highs, one might argue that there is plenty of room for more upside. That may well be – short-term market movements seldom bear any resemblance to rationality. But economic fundamentals reveal a cloudier picture, something more structural than the usual peaks and valleys of animal spirits that drive capital flows into and out of the developing world.

Growth Engines No More

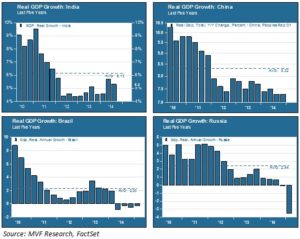

The growth question is at the top of concerns nearly everywhere in the global economy. Nowhere is this more so than in the countries recently known as the world’s growth engines. The chart below shows real GDP trends for the past five years in the four core EM economies of China, India, Russia and Brazil.

Growth is below trend in all four countries. China and India continue to do comparatively well – most countries would be thrilled to post GDP numbers in the 5-7% range. But China in particular faces a stiff set of challenges as investment, which has been the country’s principal growth driver, is slowing amid growing fears of a severe contraction in property values. Meanwhile, the dismal state of affairs in Brazil and even more so in Russia should make it clear that treating these four countries – the BRICs – as anything remotely like a single asset class theme is misguided. The problems in the BR of BRIC – brrr indeed – appear structural rather than cyclical.

Currencies and Capital Flows

The relentless upward pace of the US dollar is a problem for emerging markets in several ways. The strong dollar is driving near-record levels of EM capital outflows, which exceeded a quarter of a trillion dollars in the fourth quarter of 2014 and continue apace so far this year. For resource exporters like Russia, Brazil and Malaysia, the pain from exiting capital is exacerbated by continuing weakness in commodities prices. Meanwhile, countries with high levels of dollar-denominated debt are falling into the trap of fewer resources with which to make increasingly expensive payments. A recent report by McKinsey notes that emerging markets collectively accounted for 47% of the $49 trillion increase in debt outstanding through the end of 2013. Not all of that is dollar-denominated, of course. But, generally lacking the ability to conduct international trade in their own currencies, emerging markets are at the mercy of the dollar. There is not much mercy to be found there these days.

Breakup of an Asset Class

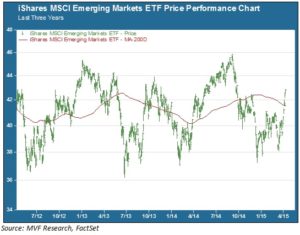

The chart below shows the boom-and-bust pattern of emerging markets equities (iShares ETF ticker EEM) over the past three years, a period in which it has spent roughly proportional amounts of time above and below its 200 day moving averae.

As the chart shows, the current price remains well below the previous highs of September 2014 and January 2013. And that last-three-years 9/14 high itself is almost 20% below the record high for EEM reached in October 2007. There may be enough momentum to propel the current rally further, but we would be inclined to proceed with caution. As we noted above, emerging markets really is no longer a single asset class. Going forward, we see more value in addressing this section of our portfolios in its component parts. Asia remains promising despite some potential road bumps along the way from China. Brazil will likely continue to be a drag on Latin America, but other regional economies including Mexico are still worth a look. As for Russia – “nyet” for the foreseeable future. Russian equities are actually going gangbusters this year. But that is coming off the trough of last year’s meltdown, and in a context where almost nothing looks good as far as the eye can see.