MV Weekly Market Flash: Goldilocks...

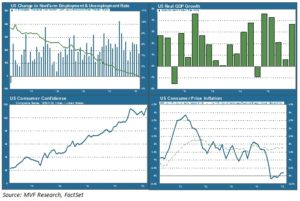

The ninth month of the calendar year is not off to a promising start for risk asset markets, as world stock indexes continue to swoon for no apparent reason. While Wall Street struggles, though, things on Main Street do not seem bad at all. The four charts below present a snapshot of a reasonably healthy US economy: steady payroll growth, decent GDP, strong consumer confidence and benign inflation. All else being equal, one would argue that the pace of recovery could take a small hike in interest rates in stride. All else never is equal, though, and the Big Question remains stubbornly unanswered, two weeks before the answer is due.

Unpacking the Numbers

Today’s job report is one of the last significant data points the FOMC will have in hand when they start their conclave on Wednesday, September 16 (awkwardly, the next CPI release comes out on the morning of the 16th, right as things are getting underway at the Eccles Building). The headline number of 173,000 new jobs is below trend, but upward revisions to June and July offset the disappointment a bit. Plus, August is a notoriously unreliable month, with frequent subsequent revisions up. Wage gains were slightly better than expected. At 2.2 percent year-on-year, wages are a bit ahead of core inflation (ex food and energy) and substantially better than the headline CPI number (which is the correct measure for comparison, since those food and energy items are a big part of household budgets). This release comes in the wake of the upwardly-revised 3.7% GDP growth and the highest post-recession reading on consumer confidence.

Juuust Right

This picture seems to resemble the “Goldilocks” metaphor so fondly invoked by the financial chattering class: neither too hot nor too cold, but just right. Too hot means we need to take dramatic action on rates to prevent rampant inflation. Too cold means groping for some kind of stimulus measures (QE4, anyone?) to get people spending and businesses investing. “Just right” should allow the Fed to get rates off the floor where they have languished since the dark days of 2008-09. And there is a reason for doing so that goes beyond the current headline numbers. Eventually, this growth cycle will run its course and the threat of recession will loom. The Fed does not want to be approaching the next economic slowdown with no room for reducing rates – that would be unprecedented and most likely not at all fun to watch. When Chairwoman Yellen expresses her conviction that raising rates is the right thing to do, it is for this reason more than it is the notion that the current economy lives or dies on the basis of a Fed funds rate 0.25 percent higher than where it is today.

Data-Driven or VIX-Driven?

The problem, of course, is that Yellen and her colleagues can’t simply pretend that asset markets don’t exist, and that their irrational tendencies don’t matter. The current volatility, along with the ongoing parade of high-profile warnings against a rate hike from the likes of IMF head Christine Lagarde and ex-Treasury Secretary Larry Summers, puts the Fed in a corner. Simply put, it will be hard for them to pull off even a very modest increase in September without roiling further the already jittery markets.

So they are likely to wait. But raising rates is necessary. We will be far more comfortable if the Fed funds rate manages to get back above three percent before this economic recovery runs its course. The bears may have the floor this month, but we hope that Goldilocks will find her voice come December.