MV Weekly Market Flash: Let...

How bad could it get? That is the question on the minds of many investors as the war in the Middle East slogs on with no apparent clarity about, well, anything. Let’s do a quick check-in to see where we are as of this somewhat rainy Friday morning in the Washington, DC environs where we ply our trade.

When In Doubt, Equivocate

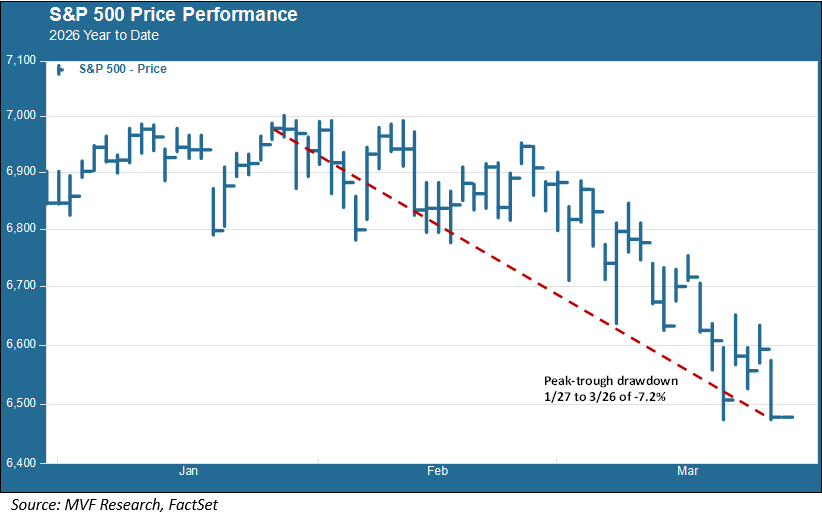

The S&P 500 stock index has lost around 7.2 percent of its value from its last record high, on January 27, to its close on Thursday. That is considerable, but the index has yet to cross either of Wall Street’s technical drawdown lines – a correction, which happens when the peak-trough reversal hits 10 percent, or a bear market, when the damage reaches 20 percent.

The relatively measured pace of this drawdown suggests that a multitude of scenarios are at play, with rosier projections imagining a near-term cessation of hostilities and eventual resumption of something approximating normal energy flows from the region to export markets, and less optimistic takes assuming that the absence of an obvious exit ramp today raises the probability of a structural quagmire. What this implies is that, within the current picture of a mid-high single digit percentage decline in stock prices, you have assumptions ranging from $200 oil to $60 oil by the time summer rolls around, with all the attendant secondary and tertiary effects in the broader economy.

About that Broader Economy

Let’s step back for a minute from the war and think about that broader economy as it exists today. We have finished tabulating corporate sales and earnings results from the fourth quarter of last year, and it was in fact a pretty good quarter. S&P 500 earnings per share grew 13.4 percent over the quarter, a much better result than the 7.1 percent consensus projection economists were making as the fourth quarter got underway. Earnings season for the first quarter of this year will kick off in a couple weeks, and here too the outlook is fairly cheery, with the EPS growth consensus currently priced in at 13.0 percent – again, this is a higher projection than earlier estimates. In other words, even with the near-certain prospect of higher inflation looming – the Organization for Economic Cooperation and Development came out this week with an estimate of US inflation rising to 4.2 percent – the consensus among economists who follow these things is that companies will continue to enjoy double-digit profits growth.

Of course, just as the price trend in the S&P 500 reflects those myriad prognostications by the Pollyannas and the Cassandras of the market forecasting world, so to do assumptions about the health of corporate earnings depend in no small part on how things fare in the Gulf. Here is one example: helium. You may have had no personal exposure to this element other than shoving a handful of helium-filled balloons into your car on the day of your three year old daughter’s birthday party. But helium is a critical input for the advanced memory and training chips employed by artificial intelligence models. The vast majority of these chips are manufactured in either South Korea or Taiwan. A large portion of the helium they need for the manufacturing process comes from – you guessed it – the Gulf region and has to pass through – you guessed it again — the Strait of Hormuz. Inventories are running low, and there have been some rumors circulating this week that Taiwan’s helium supplies were down to just a couple weeks or so.

Given that spending on AI infrastructure was plausibly the largest single driver of US growth in 2025, it obviously should be of no small concern to contemplate the possibility of significant ruptures in the supply chain that feeds AI spend (it also serves as a useful reminder that, for all the talk of a rapidly deglobalizing world, these supply chains are still very much interconnected across multiple regions and nations). This is just one example of what we mean by secondary or tertiary economic effects. A full suite of scenarios is currently at play. With time, though, the practical range of outcomes is going to winnow down, either to the upside or the downside. The decision makers responsible for whatever happens next do not have unlimited time on their side.