MV Weekly Market Flash: More...

What’s going on in the US jobs market? Over the past couple weeks, we have received a deluge of data points about job openings, layoffs, payroll gains and – the one most people think of when someone says “labor market” – the benchmark unemployment rate. What this truckload of data has not done, though, is offer a clear picture of the current state of the labor market.

Oh, and then there is one more data point, which is the tanking stock prices of a whole bunch of companies that was the subject of our commentary last week and which has spread into more industry sectors since then. We’ll get to this, which is inevitably about AI, below. But first, the headline numbers.

A Cool Front, not a Cold Front

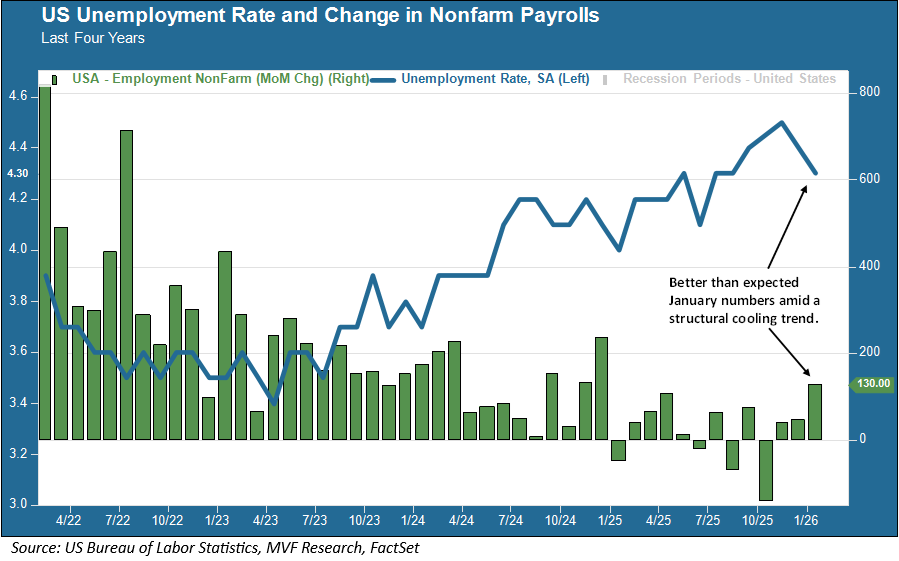

The one conclusion we can all probably draw from the above chart is that the overall trend in the labor market is cooling – it’s not heating up. Over the past four years, the unemployment rate has risen by about a percentage point, give or take, while the pace of monthly nonfarm payroll gains (the green columns in the chart) has declined. Indeed, nonfarm payrolls have declined in four months out of the total going back to January 2025. According to the revisions published this week by the BLS, the total number of job gains last year was reduced from 584,000 to 181,000. That’s a big drop.

On the other hand, the January 2026 numbers, which came out this past Wednesday, were much better than expected, with nonfarm payroll gains of 130,000 (versus economists’ forecasts of 75,000) and a drop in the unemployment rate to 4.3 percent. But there are several caveats to what appeared to be a blowout January jobs report. If history is any guide, these numbers will be revised at some point in the near future, and that could mean lopping off quite a bit from those 130,000 NFPs. Then there is the issue of where all the gains came from. It won’t be surprising to anyone who has been following the BLS reports in recent months that virtually all of the gains came from healthcare and the related field of social assistance – 124,000 jobs combined from those two sectors. Most everywhere else was some mix of slightly up, slightly down or flat.

Then there are the other recent reports from private sector sources. Perhaps the most eye-popping here was last Friday’s layoffs report from the firm Challenger, Gray and Christmas, showing that US companies posted the highest level of layoffs last month than at any time since January 2009, which you may recall was at the depths of the most brutal economic reversal since the Great Depression. Ouch. There were also some anemic numbers posted that same week by the ADP employment survey and the JOLTS report of job openings. The number of job openings, according to that report, was the lowest since September 2020 (which date should bring to mind yet another period of economic and social turmoil).

All told, then, the picture is inconsistent. Some of the numbers seem dire, others mildly negative, and a couple (e.g. the January NFPs) that one could use as a case for the “green shoots” optimistic types always like to trot out when they see light at the end of the tunnel or a similar shopworn cliché. We probably are closer to reality when we note that conditions are cool, but not yet cold.

The Ghost in the Data

But will the cooling trend stabilize, or are we about to get belted by a nasty polar vortex of labor market disruption? Many stock market investors seem to have made up their mind that the AI jobs apocalypse is here, a clear and present danger. The rout in software-as-a-service shares last week spilled over into a swath of other sectors this week including wealth management (that hits close to home) and brokerage services. The carnage spread even to some behemoths of the sector like Morgan Stanley, unlikely as it might seem that a firm of that size and stature could be brought low by some AI black box that eviscerates every legacy job in its path.

But that seems to be the vibe, thanks largely to recent product launches by firms central to the AI narrative like Anthropic and Google – these tools are apparently so incredible that they will automate everything, and the incumbent players who have been slow to reconfigure their operations from top to bottom will be shut out. To be clear, we think the current indiscriminate selling in the market is an overreaction, and shares in the companies affected will stabilize and recover at some point soon. However, there is probably at least a grain of truth in the potential these AI tools have to threaten the livelihoods of workers in these and other industries. It would be wise not to take too much comfort in the January job numbers as a sign of green shoots.