MV Weekly Market Flash: Political...

Over the past couple weeks we have been snooping around some of the contrarian corners of the world, to see what those folks not completely enamored of the “Trump trade” have been up to (Eurozone, Brexit, what have you). While we were away, all manner of things has gone down in Washington, often in a most colorful (or concerning, take your pick) fashion. But virtually all the chief planks of that Trump trade – the infrastructure, the corporate tax reform – remain stuck in the sketchbooks and doodlings of Paul Ryan and his band of policymakers, waiting to see the light of day. By this point in his first term, Barack Obama had already passed a $1 trillion stimulus bill, among other legislative accomplishments. Is there a point at which the band of inverse-Murphy’s Law acolytes begin to question their faith that if something can go right, it will? To put it another way, does political risk still matter for asset valuation?

“Vol Val” Alive and Well

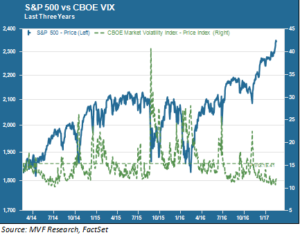

If there is a political risk factor stalking the market, it appears to have paid a call on J.K. Rowling and come away with a Hogwarts-style cloak of invisibility. For evidence, we turn to our favorite snapshot of trepidation and animal spirits – those undulating valleys of low volatility occasionally punctuated by brief soaring peaks of fear that make up the CBOE VIX “fear gauge,” shown in relation to the price performance of the S&P 500.

Since the election last November, market volatility as measured by the VIX has subsided to its lowest level since the incredibly somnambulant dog days of summer in 2014. In fact, as the chart shows, the lowest vol readings have actually occurred on and after Inauguration Day (so much for that “sell the Inauguration” meme making the rounds among CNBC chatterboxes a few weeks back). Meanwhile, of course, the S&P 500 has set record high after record high. How many? Sixteen and counting, to date, since November 9, or about one new record for every four days of trading on average.

That by itself is not unheard of though: the index set a new record 25 times (measured over the same time period) following Bill Clinton’s reelection in 1996. But 1996 was a different age, one with arguably less of the “this is unprecedented” type of political headlines to which we have fast become accustomed in the past two months. To a reader of the daily doings of Washington, it would seem that political risk should be clear and present. One of this week’s stories that caught our attention was the good times being had by London bookmakers setting betting markets for the odds of Trump failing to complete his first term (the odds apparently now sit around 2:1). So what gives with this week’s string of record highs and submerged volatility?

The Ryan Run-up

The “Trump bump”, of course, was never about the personality of the 45th president, or anything else that he brings to the table other than a way to facilitate the longstanding economic policy dreams of the Ayn Randian right, represented more fulsomely by House Speaker Paul Ryan than by Donald Trump. Looking at the rally from this standpoint perhaps explains at least in part the absence of visible political risk. So what, goes this line of thinking, if Trump were either to be impeached or somehow removed under the provisions of the 25th Amendment? Vice President Pence ascends to the Oval Office, the Twitter tornadoes subside and America gets on with the business of tax cuts and deregulation in a more orderly fashion (though not much infrastructure spending, as that was never really a Ryan thing). Move along, nothing to see here.

While we understand the logic behind that thinking, we think it is misguided, not least of all because – London oddsmakers notwithstanding – we think that either impeachment or a 25th Amendment removal from office are far out on the tail of any putative distribution of outcomes. We would ascribe a higher likelihood to a different outcome; namely, that political uncertainty will continue to permeate every sphere of activity from foreign policy to global trade to domestic unrest in a bitterly divided, partisan nation. So far we are muddling through – headlines aside, many American institutions are showing their resilience in the face of challenge. That’s good news. But not good enough, in our view, to keep political risk behind its Invisibility Cloak for much longer. We’re not prophesying any kind of imminent market cataclysm, but we do expect to see our old friend volatility make an appearance one of these days in the not too distant future.