MV Weekly Market Flash: Populists...

You may recall, dear reader, that there was a national election in Italy back in March that proved to be highly inconclusive. We’ll give ourselves a modest pat on the back for prognosticating ahead of that event its most likely outcome – a non-decision with power hanging in the balance as ascendant populist parties try to figure out a workable cohabitation while the previous center-left government – here as elsewhere throughout Europe – fades into oblivion. That election returned to occupy market attention this week.

Not This Time

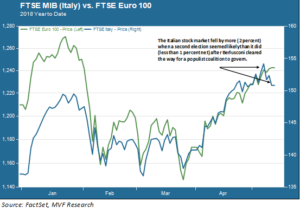

The string of recent elections in Europe that started with the Netherlands and France around this time last year, and continued on into Germany last autumn, managed in each case to avoid a decisive populist surge into power while at the same time underscoring just how unpopular traditional parties there are – particularly those of the once-dominant center-left. At some point, the run of dumb luck was due to come to an end. That seems to have happened. It remains to be seen, though, whether the increasing likelihood of a government variously hostile or (at best) indifferent to the EU and the single currency will unnerve investors. Despite a bit of a hiccup on the Milan bourse (shown in the chart below) and a slight widening of the spread between Italian benchmark bonds and German Bunds, the answer so far is – not much.

Voi Volete Governare?

The question left pending after the March election was whether any such “workable cohabitation” for governing would be possible between the party platforms of the Five Star Movement (FSM) – the creation of a popular comedian, Beppe Grillo, the unifying message of which seems to be nothing more than “throw all the bums out” – and the more ideological Northern League, an ethno-nationalist party with roots in a movement for Italy’s prosperous north to secede from the rest of the country. As early as Tuesday this week that question appeared unresolved, and the chatter turned to the embarrassing possibility of a second election just months after the first.

Send In the Clown

Then, on Wednesday, the contours of Italy’s next government became clearer. Former prime minister and walking evidence for why the #MeToo movement exists, Silvio Berlusconi, gave his tacit blessing to a League-FSM governing union. Berlusconi’s own Forza Italia party underperformed in the March elections, but retained enough clout to give its still-politically viable leader a kingmaker role. The respective leaders of the League and the FSM, Matteo Salvini and Luigi di Maio, have instructed their key staff to reconcile platform positions by the end of the weekend. There is still the possibility that these will not bear fruit, but the consensus among insiders familiar with the process is that the next government of this G-7 nation will be run by a coalition decidedly at odds with Brussels on many important issues ranging from immigration to Eurozone fiscal policy to the need for sanctions against Russia (like many other European populist movements, both the FSM and the League are generally pliant towards Russia and Putin).

Nothing to See Here…Yet

There is a grain or two of rationality in the market’s relative complacency towards Italy. On the bond side, the ongoing presence of the ECB is a strong counterweight against wild fluctuations in yields. The central bank holds about 15 percent of the total float of Eurozone sovereign debt, which creates stability. The return to stagnation in the Eurozone economy (see last week’s commentary) reduces the likelihood that the ECB will move soon in any drastic way to curtail its QE program.

In equity-land, the large cap Italian companies that account for the lion’s share of total tradable market cap are largely multinationals with a diverse geographic footprint and thus less directly exposed to a potential economic downturn in their home market.

The current sense of calm notwithstanding, investors have long wondered whether a populist/nationalist government at the head of one of the major Eurozone nations poses a critical threat to the viability of the single currency region. An answer to that question, one way or the other, may be forthcoming in the months ahead.