MV Weekly Market Flash: Recession?...

Remember August? Just one month ago, the financial village was all abuzz about the R-word: the recession that seemed to be all but inevitable. Equity markets swooned, but the big story was (as tends to be the case in this day and age) in the bond market. The volume of debt trading at negative interest rates soared, the yield on the US 30-year Treasury fell below 2 percent for the first time ever, and the yield curve inverted between the 2 and 10 year notes. That latter development, the economists reminded us, is the surest sign of all that a recession is coming.

Convincing, Except for the Data

Then along came September. It has not been an uneventful month for assets thus far, to be sure. There was the Great (Non) Rotation that was the subject of our commentary last week, a big back-up in bond yields, sudden volatility in oil prices following the attack on Saudi Aramco’s production facilities last weekend, and weirdness in the overnight lending market this week (we’ll have more to say about that below). But those recession fears of August have faded into the background. Could part of the reason for that be that the data simply continue to suggest a low threat level for a downturn?

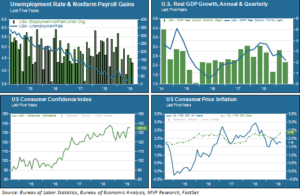

Let’s check in with the chart you will have seen if you read our quarterly State of Play presentations – a snapshot of four key macroeconomic data points, those being employment trends, real GDP growth, consumer confidence and inflation.

We should stress that none of these indicators promise that we won’t have a recession – macro data tell us what has happened, not what will happen. Still – with consumer confidence still close to decades-long highs, a consistently healthy job market and even a slight uptick in core inflation, our longest recovery on record seems robust enough to keep going for at least another few months. Meanwhile that ominous 2-10 inversion on the yield curve has abated, with that portion of the curve more or less flat at this point.

Credit Markets Rumble

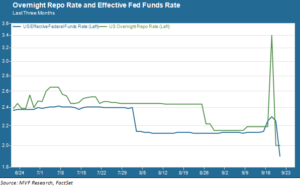

So if recessionary fears have cooled and restored some calm (on the surface at least) to equity markets, what factors could bring October tricks to upend September treats? We return, unsurprisingly, to the credit markets, home of much that is weird in our world. This week, the weirdness took place in the usually dull overnight lending market – specifically, the market for repurchase agreements (“repos”). This past Tuesday the overnight repo rate did something very strange: it shot up for no apparent reason. The chart below shows the repo yield along with the Fed funds rate. As the chart makes clear, the repo rate normally tracks the effective Fed funds rate very closely. Until…

On the first day of the September FOMC meeting – a meeting where the Fed was widely expected to lower rates – the overnight repo rate shot up (at one point as high as 10 percent in intraday trading). The next day it plummeted down below its previous levels as the Fed did, indeed, reduce the Fed funds rate by a quarter percent at the Wednesday conclusion of its meeting. Investors with memories of the chaotic market conditions for overnight securities in 2008 were briefly spooked by this bizarre pattern.

The repo mystery turned out to have a fairly straightforward answer: supply and demand. Money market funds are a major player in the repo market as a source of cash. There was a large cash outflow from money markets at the end of last week as corporations paid interim taxes ahead of a September 15 deadline. At the same time, there was a $54 billion settlement of previously auctioned Treasury securities on Monday, creating an unusually high demand for cash. The Fed stepped in with an infusion of $75 billion three days in a row to ease the supply-demand imbalance, which has had the desired effect. There was no real spillover of any kind into other asset classes.

That’s the good news. The bad news is that the imbalance happened in the first place, because it suggests that bank reserves and other go-to sources of readily available cash are not present in the system at the levels they should be. That problem, in turn, reminds us that after ten years of wildly unconventional monetary policy leading to swollen central bank balance sheets, negative interest rates and all the rest, we are navigating the credit markets in an obscuring fog.

The good news is that the Fed will probably reconfigure its repo facility to mitigate the likelihood of another supply-demand hiccup like the one we saw this week. Central banks have learned that flexibility to adapt to changing circumstances is their number one responsibility – and they generally carry it out well. But they are not omniscient, and the complexity of the credit market’s thousands of interacting mechanisms defy are not reducible to easy answers.

Central bankers have a toolkit for fighting recessions. It’s how the more unconventional of these tools can affect the financial system in unexpected ways that is a bigger concern than a recession itself.