MV Weekly Market Flash: Retail...

2014 was a year of both higher job growth and consumer confidence, which in turn helped boost retail sales for most of the year. A post-recession high for December consumer confidence, in conjunction with lower gasoline prices, should be a winning combination for more discretionary spending amongst consumers. However, the retail sales data that came out on Wednesday showed a -0.9% decline as well as a downwards revision to the previous release of the strong November numbers from a 0.7% advance to 0.4%.

This brings about the biggest drop in retail sales since last January. Not surprisingly, gasoline stations had the largest decline among the retail sectors with a -6.5% drop (falling oil prices mean gas stations are making less money). We would expect a gas windfall to produce a big bump in middle class spending, but consumers’ savings at the pump don’t seem to be translating into spending elsewhere yet.

The retail sectors that grew in the month of December are arguably the more “staple-like” sectors: food and beverage, furniture and home furnishing, and health and personal care. In contrast, some of the hardest hit retail sectors were clothing stores, motor vehicles, and electronic stores.

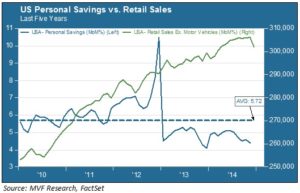

Let’s step back from the December figure and consider the larger context. Over the past five years retail sales have grown steadily, while the household savings rate has declined slightly. In 2014 savings fell somewhat more notably, but at the same time the rate of retail sales growth tapered off and in fact was lower than at any time since the end of the recession. This could be a sign that households are doing things with their savings other than going to the mall – paying down debt, perhaps. That may be the signal we are seeing from the December retail number. It also may tie into the stagnation in wage growth we highlighted in last week’s market flash.

Another factor to consider is that maybe the American consumer’s behavior is beginning to change. As noted above, retail sales growth for the year is the lowest that we have seen since we were in the midst of a recession in 2009, which is especially interesting considering that 2014 has been the best recovery year since the recession ended. And although we saw one of the most successful Black Fridays of all time this past November, consumers – and even retailers – showed a noted (if perhaps only anecdotal) reversal in attitude towards the overt commercialism of the day. More and more shoppers are forgoing the mall for their computers to shop, and the holiday season cash cow – where retailers have traditionally made the majority of their yearly earnings – is changing. How this change will impact the broader economy is still a work in progress.

Monthly leading indicators can provide a good spot check on the economy, but are oftentimes misleading as they are subsequently revised and provide a data snapshot of just one month. All in all, we don’t feel that December’s disappointing retail sales numbers are anything to fret over, but we shouldn’t ignore them completely. Traditionally consumer spending drives the US economy as the highest component of GDP. If consumer habits are indeed changing, the very basis of the economy and the way it operates will likely be changing along with it.