MV Weekly Market Flash: Still...

Animal spirits are running high in the month of March to date. A whole dealer’s choice of assets ranging from global stocks to crude oil to the South African rand and Turkish new lira are all climbing out of the depths of despair in which they had been mired for most of the first two months of the year. For the time being, anyway, it appears to be a moment for the long-suffering to shine. While emerging markets and energy & production stocks have their day in the sun, the so-called “Nifty Nine” and other darlings of 2015 languish. The MSCI Emerging Markets index is up 5.4 percent since the month began, and more than thirteen percent above the six and a half year low point reached back on January 21. Bargain hunters quite naturally sniff a deal: is it one worth taking?

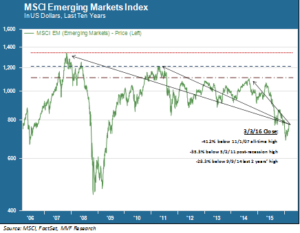

The Rally in Context

Thirteen percent is nothing to sneeze at, but it remains a long way even from relatively recent high water marks. The chart below illustrates the price performance of the MSCI Emerging Markets index over the past ten years. The dotted horizontal lines represent, respectively, the pre-recession all-time high (2007), post-recession high (2011) and last two years’ high (2014).

Investors viewing emerging markets from a tactical standpoint would probably look with most interest at that last two years’ number: even after the recent rally, the index is still more than 28 percent away from the L2Y high point reached in September of 2014. That’s a lot of ground, which arguably means that tactical investors could take comfort in not having missed the boat. Double-digit annual gains would not necessarily be out of the question with the right combination of EM-friendly tailwinds.

Not Much New Under the Sun

Chief among those tailwinds would likely be a continued run-up in energy and industrial metals prices, a strengthening of local currencies against the US dollar, and a general absence of bad-news surprises principally from China, but also from other suffering EM locales including Brazil and Russia. A glance at the headlines in the month to date, though, suggests that not much has really changed in the fundamental landscape of the global economy. The recent rally in crude prices, arguably (if unusually) the principal catalyst in equity strength, is based less on a real improvement in the global supply-demand balance than on atmospherics about what oil ministers will say to each other when they (supposedly) meet later this month. China’s recent headline numbers have been less than impressive, including capital outflows, weak industrial production and sagging imports and exports. Brazil’s recession is turning deeper than expected, while the ongoing Petrobras political scandal has now ensnared the country’s former president, Luiz Inácio Lula da Silva. Perhaps the brightest recent news tidbit from emerging markets comes from the unlikely source of Argentina. That longstanding pariah appears ready to return to the capital markets after the new government of Mauricio Macri settled a longstanding debt dispute with major creditors earlier this week.

In our commentary last week we suggested not getting too comfortable even while enjoying the fruits of the recent global equities rally. We would extend that cautionary note even more emphatically to emerging markets. While the above chart shows enticing new ground to break on the upside, there is plenty of potential downside as well. In a market environment driven largely by whichever lurking X-factors pop into or out of existence like so much antimatter, the next big move could be either way.