MV Weekly Market Flash: The...

So, everything’s back to normal, right? The sharp pullback that began with the hourly wage number exactly two weeks ago has assumed its usual V-shape, with 5 straight trading days in the green following the technical correction level of minus 10.2 percent reached on February 8. Just like that silly Ebola freak-out back in 2014, this one looks like it will pass over, a brief squall yielding back to calm seas without so much as a full day spent below the 200-day moving average.

Right?

Yields Go North, Dollar Goes South

The good news, for those who prefer their equities portfolios neither shaken nor stirred, is that the continuing rise in bond yields is failing to inject fear into risk-on asset classes. The 10-year Treasury yield broke through 2.9 percent on Wednesday, even as the S&P 500 recorded yet another intraday gain of more than 1 percent. Those inflationary fears would seem tempered, even though Wednesday’s news cycle also served up a core CPI growth number a bit higher than consensus expectations. For the moment, anyway, the stock market seems comfortable enough with higher rates.

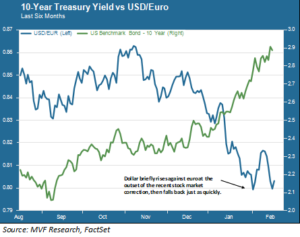

Which brings us to today’s big question: what is up with the US dollar? The chart below shows the downward trajectory of the dollar against the euro over the past six months, during which period the 10-year yield soared from just over 2 percent to the recent 2.9 percent.

All else being equal, rising rates should make the home currency more, not less attractive. Investors prefer to invest where returns are higher. Moreover, the dominant economic narrative around the US for the past half-year or so has been positive: above-trend growth, strong corporate earnings and high levels of business and consumer confidence. What’s not to love? Yet, even while the spread between the 10-year Treasury and the 10-year German Bund is 0.45 percent wider than it was six months ago the euro, as seen in the chart above, has soared against the dollar. And the pace has only accelerated since the beginning of 2018. Yes, the dollar jumped ever so briefly as a safe haven mentality took hold two weeks ago, but it fell back just as quickly – even while the 10-year yield reached new 4-year highs.

Supply and Demand, Yet Again

We’re starting to feel like Econ 101 professors around here lately, given how often the phrase “supply and demand” shows up in our commentaries and client conversations. We think it may be the single most important catchphrase for 2018, and in it lies a plausible explanation for that odd relationship between the dollar and bond yields. The supply-demand road inevitably leads back to China.

China’s central bank buys US government debt – lots of it. Chinese foreign reserves exceed $3 trillion, and the vast bulk of those reserves exist in the form of US government securities. Two things happen when Chinese monetary authorities (or any other foreign institution) buy US paper, all else being equal. First, the price goes up, and thus the yield, which moves in the opposite direction of the price, goes down. Second, the dollar goes up because Treasuries are a dollar-denominated asset. You see, it really is all about those supply and demand curves.

Recent evidence (including a weak Treasury auction last week) suggests that Chinese Treasury purchases are somewhat lower than they have been in recent years. That rumor back in early January, though quickly disputed, may have a kernel of truth to it. Foreign buyers indeed may have less appetite for Uncle Sam’s IOUs. Maybe they expect more inflation down the road (which would assume higher nominal rates). Maybe other factors are afoot. Whatever the reasons, reduced demand from non-US sources would indeed have the likely effect of pushing up rates and pushing down the dollar at the same time.

If this is the case, then we may be in for more bumpiness in equities. The S&P 500 digested the move to 2.9 percent very smoothly. We may see in the coming weeks whether the story plays out the same way at 3 percent or more. There will be a truckload of Treasuries coming down the road as we borrow to fund all that new spending and those tax cuts. More supply, in other words, potentially chasing less demand.