MV Weekly Market Flash: The...

There will, probably, be a time again when it will make sense to have a significant allocation of non-US equity indexes in one’s investment portfolio. But that time, in our considered opinion, is not today.

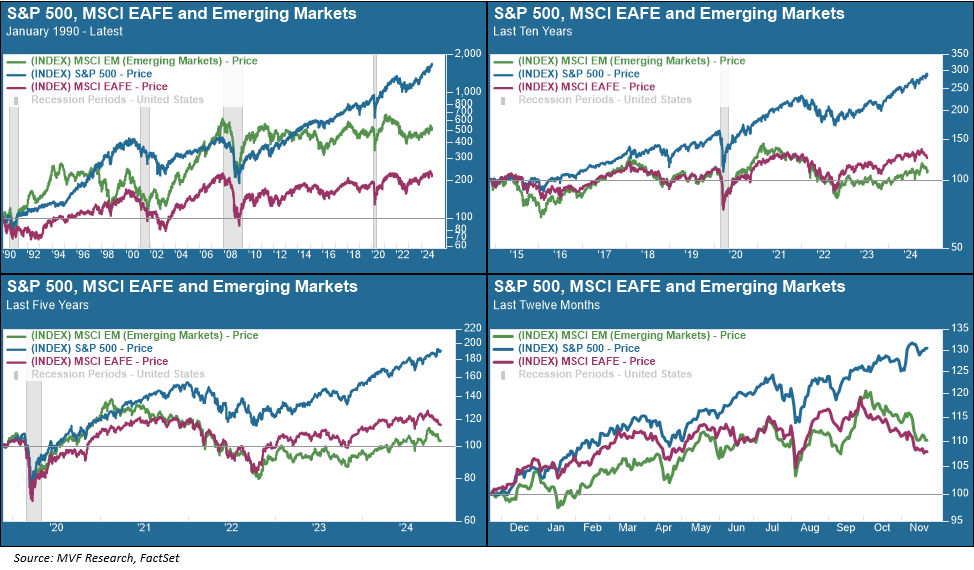

As the end of the year approaches, our primary focus as always turns to our asset allocation choices for the year ahead. Some years can elapse quietly with minimal tweaks to portfolio weights, while others require extensive rethinks on a more frequent basis. We imagine that 2025 will fall into the latter category. Fair warning: our model portfolios in June may look quite different from their appearance in January. Maybe that rethink will include a fresh take on non-US equities. But nothing today is telling us to expect a shift away from what has been perhaps the single most enduring advantage in equity allocation for several decades now, and that is US large cap equities. Consider the evidence, as shown below over multiple long, intermediate and short time periods.

The upper-left quadrant in the above chart sums it up neatly: if you had invested $100 in the S&P 500 index of large-cap US stocks in 1990, that $100 would be worth $1,683 today. Had you opted instead to invest it in emerging markets (via the MSCI Emerging Markets index, shown in green) your investment would be worth $505 today. Moving on down, a decision to go with developed economies outside the US, here represented by the MSCI EAFE (Europe, Australasia and Far East) index, would leave you with just $216 today, thirty-four years later.

And that’s without taking risk considerations into account. Both non-US indexes (particularly emerging markets) exhibited a higher level of volatility over this period than the US, turning on its head the traditional mantra of “higher risk for higher return” that the finance textbooks teach us. The US advantage has held up consistently in shorter time periods as well, right down to the last twelve months. As the chart in the bottom-right quadrant shows, the S&P 500 in 2024 maintained its advantage throughout a year which many in the financial chattering class thought would finally mean-revert to favor non-US opportunities.

The root causes of this enduring advantage are several. We think two of them offer the most convincing explanations: first, the dominance of information technology in domestic US indexes; and, second, the flatlining of the China supercycle from the mid-2010s as the world’s second-largest economy failed to rebalance towards a more equitable distribution between industrial production and consumer spending. Let’s take each of these in turn.

US large cap equity indexes are dominated by a small number of technology companies that own a vast amount of the intellectual property that powers our economy. This intellectual property is pervasive across the entire spectrum of industry sectors from finance to retail to manufacturing. There simply is no comparable pool of high-tech IP present in the equity indexes of our peer developed economies. Information technology makes up less than nine percent of the EAFE index by sector weight, compared to 31 percent of the S&P 500. And that’s not even counting the contribution of four companies – Alphabet (Google), Meta (Facebook), Amazon and Tesla that are technically not part of the “information technology” sector (Alphabet and Meta being constituents of the communications services sector while Amazon and Tesla reside in the consumer discretionary sector). Those four companies alone make up twelve percent of the S&P 500’s market cap, in addition to the 31 percent in the IT sector.

Over in the world of emerging markets, it has largely been a story of China and everybody else, at least until recently (we have our eyes on India as a potential challenger). In the 1990-present chart above (upper-left quadrant) you can see the effect the China supercycle in its heyday had on the emerging markets index, from roughly 2002 to 2012. China came out of the 2008 global financial crisis in a stronger position than most of the developed world and seemed well-positioned to make a serious challenge for global leadership. But that all stalled out in the middle years of the 2010s as Beijing’s economic policymakers made several half-hearted attempts to rebalance the economy and bring its consumer spending component more closely in line with that of other countries. It never managed to pull it off, always reverting back to the tried-and-true formula of increased spend on manufacturing and, especially, property development. The Chinese property market today is in a slow-burning collapse, with its largest enterprises bankrupt or in serious financial trouble, and its discontented homeowners shutting down their monthly household expenditures. The economy is dangerously close to tipping into a deflationary cycle reminiscent of Japan in the late 1990s and early 2000s.

These structural challenges to both developed and emerging non-US markets would have been present regardless of how the recent US election went, with the attendant implications of trade hostilities, tariffs and sanctions replacing the seemingly bygone world of free trade and open borders. Those only add to our conviction that now is not the time to be making a meaningful move into non-US equities. This all may change, and probably will, sooner or later. But not yet.