MV Weekly Market Flash: The...

This week we got two seemingly contrasting readings on the state of play in early 2014, and what may be in store for investors, businesses and households this year. The stock market pulled back, with the S&P 500 extending its loss for the year to date north of 4% by early Friday morning trading. The U.S. economy, on the other hand, produced another positive data point, with the first reading of 4Q GDP coming in at 3.2%.

This is less odd than it may seem, and very much consistent with our base case scenario for the year. The stock market is expensive, even with the recent pullback, and prone to potentially more bouts of selling. The fundamental economic picture, though, continues to show more promise than reasons for fear. That may not be enough to produce another year of double-digit equity returns. It may be enough, though, to make a good case against things getting too negative for long-equity portfolios.

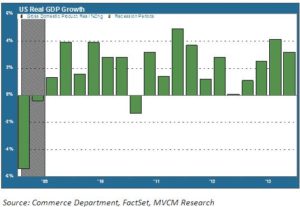

GDP By The Numbers

A look at the chart below shows three consecutive quarters for GDP above the critical 2% level. Economists believe that the economy needs to grow at a clip of 2.5% or better to generate net new jobs (i.e. where job growth outstrips population growth). A string of readings above this level increases the potential for the unemployment rate to fall for the right reason – new job creation – rather than the wrong reason of decreased labor force participation. That wrong reason was the driving force in last month’s surprise fall from 7% to 6.5%.

Let’s look at where the growth came from, because there are some interesting storylets below the top line. The biggest contributor was consumer spending, accounting for 2.3% of the total. That’s unsurprising: in Shopaholic Nation, consumer expenditures typically make up about 70% of GDP. What is unusual is the next largest line item on the national account: net trade. The balance of exports over imports contributed 1.3%. This dovetails with the decreasing U.S. trade deficit we described in a previous Market Flash, but still is surprising given weakness in emerging markets and a stronger U.S. dollar. Net housing and business investment was up a modest 0.6%.

Take That, Government Shutdown!

So add up all those figures – 2.3%, 1.3% and 0.6% – and you get 4.2%. So why did GDP only grow by 3.2%? The wet blanket on the party was government spending, which subtracted 1% from the equation. Remember last October? The shutdown, the flirtation with disaster as posturing policymakers played chicken with the government budget and with the debt ceiling? That proved to be the weak link. The good news, though, is that even with this fiscal drag the economy was still able to grow by more than 3%. The even better news is that there is likely to be less fiscal drag this year than last. Congress managed to reach a budget deal by the end of last year, and this year even the partisan muckrakers may be a bit more tempered in their actions ahead of the November midterms.

Where Do All The Profits Go?

There are a couple cautionary notes in the generally positive picture, though. First, this reading is subject to revisions. That could impact the seemingly-too-rosy net trade numbers. Second, business investment results are not particularly impressive. Half of business investment came from inventories, as opposed to investment in new productive assets. Profits for U.S. businesses have been robust for many years, so what are they doing with all that money? Anyone who follows quarterly corporate earnings announcements knows the answer: it’s going back to shareholders in the form of share buybacks and dividends. The dividend payout ratio at a number of large S&P 500 firms is over 100%. That means the firms pay out 100% of their net earnings in the form of dividends and buybacks, and then borrow more money to pay out even more! Why not, the thinking goes, given today’s low interest rates?

Push Me, Pull You

Finally, this latest uplifting data point brings the Fed’s rate policy back into the picture. Short term rates soared after the Fed’s December meeting on doubts about whether the extended forward guidance target was realistic in a faster-growing economy. Then rates fell sharply after the surprisingly negative jobs report in early January. Now they may rise again, then they may fall again in a credit market version of push me – pull you. We need to keep a close eye on this. But on balance, we will prefer to see a stronger economic picture continue to take root. Heaven forbid, that might actually take us back to a world where equity fundamentals matter more than the word “taper”.