MV Weekly Market Flash: The...

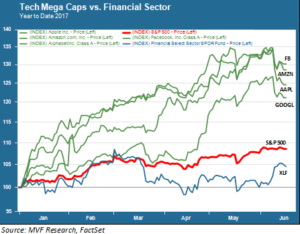

Investors tend to be predisposed to a “follow the leader” mentality — to latch onto a narrative that purports to explain why company ABC or sector XYZ is running out ahead of the pack. Unfortunately for those in search of a leadership theme on the cusp of the summer of ’17, there really isn’t one anymore. There was one until last week: the mega cap stocks led by Facebook, Amazon, Alphabet (Google) and Apple took the helm back in the first quarter as the “reflation trade,” the previous narrative, faltered. The chart below shows the ascendance of these FAGA stocks when financials, the reflation trade’s leader, turned south in March (represented by XLF, the SPDR ETF). The chart also shows the carnage of June 8, when those high flying mega caps suddenly got pummeled on an otherwise nondescript trading day. They have continued to struggle in the days since.

MAGA…

The fizzling out of the reflation trade (or the “Trump bump” in the vulgate) as a leadership theme is easy to understand. The financial sector led that narrative, along with materials, industrials and (for a while late last year) energy. The premise was that a burst of pro-growth fiscal policy, headlined by tax reform, deregulation and a massive infrastructure stimulus would unleash an inflationary tsunami. Financial institutions would benefit from improved net interest margins, while industrial producers and resource firms would ride the infrastructure bandwagon. That premise, never particularly strong in a reality-based sense to begin with, looked increasingly like a bad bet as the legislative degree of difficulty presented itself to a team of political novices. Financials and other reflation-theme names topped out in early March and the broader market drifted for a spell.

…to FAGA…

FAGA (the aforementioned mega cap stocks) and their fellow travelers in the tech sector picked up where the Trump trade left off. What was the narrative driving this leadership rotation? Little, in our opinion, other than a general go-to argument that these enterprises are part of an elite cohort able to deliver consistently fast top-line growth in a world of modest economic prospects. The FAGA trade is sort of a lazy, modern take on the “Nifty Fifty” of days yore: in the absence of any other overarching narrative, go with the brand-name leaders of the day. And what, exactly, was the catalyst for that mass exodus from FAGA on June 8? Again, nothing that is glaringly obvious. Pundits put forth the “crowded trade” theme, which may be as good a reason as any. But they are not especially overvalued; Apple still trades at a P/E discount to the broader market, and the P/E premia of the other three FAGA names to the S&P 500 are well below their highs for the past five years.

…to TINA

Whatever the reasons were for bailing from tech on June 8, it is by now evident that it was not a one-day event; the sector has underperformed in the days since, as the above chart illustrates. The question now turns to the prospects for the broader market absent another leadership story. Candidates for such a story are rather scarce. The many ills plaguing the retail sector again came into sharp relief this week when supermarket chain Kroger’s radically cut its earnings outlook and saw its stock price get beaten down more than 18 percent. Healthcare waxes and wanes amid a fog of fundamental, sector-specific uncertainties. Financials face the headwinds of lower than expected inflation and the attendant opinion by many that the Fed was mistaken to move ahead with its rate cut this week.

The antidote for the confusion is TINA – There Is No Alternative. Forget the Trump trade, or tech stocks, or any other leadership narrative. It’s enough, this argument goes, to stay in the market when there are no compelling reasons to get out. As long as there is growth, however modest, and as long as there are central banks with the means to limit the downside, there should be no need to start building up the cash position. That logic has served investors well to now. But watch those narrowing spreads between short and intermediate term bonds. They don’t necessarily signal anything in terms of a major market shift. But they are not moving in the right direction.