MV Weekly Market Flash: The...

Let’s talk about those GDP numbers. But let’s also think about how Wednesday’s report on GDP from the Bureau of Economic Analysis – in the parlance of economists a “hard data” report – relates to Tuesday’s release of the latest Consumer Confidence Index from the Conference Board. Confidence is a human sentiment, and thus survey data like the Consumer Confidence Index fall into the category of “soft data.” Up until this week, these two different macro data categories were telling two different stories about the economy. The hard data – growth, inflation, jobs – were mostly okay, reflecting continuation of the solid progress on all fronts made by the US economy in 2024. But the sentiment data, as told by the Conference Board, or the University of Michigan consumer sentiment index, or the National Federation of Independent Businesses (NFIB) survey of sentiment among small business owners, were steadily declining throughout the first four months of the year. Negative sentiment, in other words, was running ahead of the still-okay hard data.

One of These Is Not Like the Others

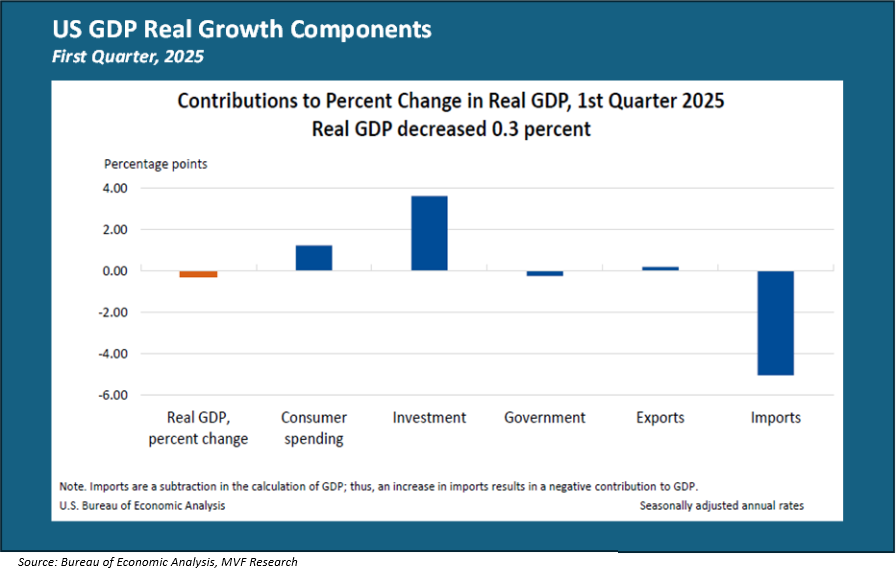

Eventually, of course, the sentiments that drive spending, saving and investment decisions by households and businesses are going to show up in the hard data, in the form of units of economic goods that either get sold or don’t get sold, at a higher price or a lower price, by enterprises that either are or are not running production lines at some high or low fraction of full capacity. One such “soft” sentiment showed up loud and clear in the Q1 GDP report. See if you can spot what category it influenced in the chart below.

If you guessed “imports” then you are spot on. A major surge in imports was the driving force behind the negative percentage change in real GDP. Imports, as the small print on the chart supplied by the BEA notes, are a subtraction to GDP. If “net exports” – exports minus imports – is negative, then the contribution to GDP is negative. Clearly, the miniscule amount of US exports in the first quarter was overwhelmed by the massive amount we imported, and the net result was the headline number of minus 0.3 percent growth that dominated the financial chatter on Wednesday.

The good news is that we probably won’t see another quarter of imports at this level, so the Q1 report is not a clear signpost to successive quarters of negative growth. Consumer spending remained positive (though at lower levels than 2024) and private sector business investment advanced by nearly four percent, so at least for now, the underlying picture is of a slowdown, not a collapse.

Hoard Today, Hibernate Tomorrow

The bad news is that the surge in imports can almost entirely be ascribed to the negative expectations businesses have about the economic environment for the rest of the year (expectations are a big part of the aforementioned sentiment indexes). With tariff announcements continuing to wax and wane on a near-daily basis, and the first practical signs of their effect coming into sight in the form of shipment levels and transportation prices on major trade routes between Asia and the US, businesses have been making the logical decision to front-load their purchasing needs before prices go up and supply chains break down. They are hoarding ahead of a perceived economic winter, and that carries negative implications for activity later in the year.

Can we quantify those negative implications? No, given that at this point it’s anybody’s guess what tariffs are in place today, what ones will be in effect tomorrow, and how other countries are going to respond with their own adaptive strategies. It’s a tough time for anyone trying to make economic forecasts – witness the number of companies basically scrapping their forward guidance as they report on first quarter earnings. But those “soft data” sentiment numbers carry a very clear message from households and businesses: don’t just pay attention to what we say, but watch what we do.