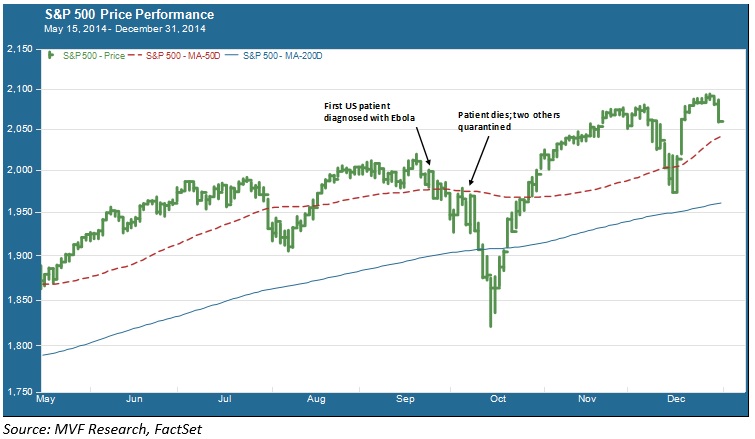

MV Weekly Market Flash: What...

Back in August of 2014 the World Health Organization issued a Public Health Emergency of International Concern statement in relation to a viral disease that had been spreading among the populations of a number of West African nations for the past several months. The disease was called Ebola. Apart from the affected areas and the international health organizations involved in trying to stop its spread, Ebola garnered little attention from the world at large. Then, in late September, a US citizen returning from Liberia to Dallas, Texas contracted the disease and, after some misdiagnosis from the local hospital, was eventually quarantined and died in the first week of October. US stock markets wobbled a bit. Then, two nurses who had attended the deceased patient were also diagnosed with the disease and quarantined. Markets went from wobbly to full panic mode in the space of a day or two. The chart below shows the S&P 500 during this period.

The market panic over Ebola was swift and, for a one-off event, relatively deep: the S&P 500 was down more than 7 percent from its previous peak when it just as abruptly bottomed out and staged an impressive recovery, setting one record high after another through early December (notably, the two nurses who were quarantined both survived as did one further US-based Ebola patient). The emergency edict issued by the WHO was still in effect, but the health risk to people (or business enterprises) outside the West African nations at the center of the outbreak was judged to be relatively limited.

A Different Virus in a Different World

In the early weeks of 2020 we are in the throes of another international health scare. This week the World Health Organization issued another Public Health Emergency of International Concern in regard to the coronavirus that has spread from its origination point in Wuhan, China to more than 10,000 cases worldwide (including the US). Clear evidence of person-to-person transmission has been recorded. China has responded with an effective quarantine of the city of Wuhan, travel in and out of China more broadly has been severely restricted, and the Chinese economy – the world’s second largest – is clearly feeling the impact. Starbucks, which has a huge operation in China, has closed half its stores there. Other US and global firms with significant Chinese assets have also taken direct action. Given the economic size of this disease’s epicenter, it would seem like cause for greater concern among global markets.

And yet, the reaction thus far has been relatively muted. At its lowest point since the coronavirus first became news the S&P 500 was down just 2.5 percent from its recent high (and since last fall the US blue chip index has set one record high after another). Even Hong Kong’s Hang Seng index, right in the thick of exposure to mainland China and still burdened with its own problems of domestic unrest, has lost less in percentage terms thus far than US markets did during that brief Ebola panic. In general, world markets seem less prone to sudden panics than they were six years ago. Is that a sign of maturity, or a misreading of the risks at play?

Not Default to Worst

The market’s spasm of panic during the Ebola scare seemed to be a knee-jerk default to the worst possible outcome – an uncontrollable pandemic. This time around the market response seems more suited to the magnitude of the event, at least given what we know to date. Yes, this is a serious viral outbreak and yes, the main country involved is an economic giant. But so far there is no compelling evidence that it is verging towards being uncontrollable. The WHO has assessed China’s response to the outbreak in mostly positive terms, noting the number of medical facilities the authorities have constructed in a very short time period and the pragmatic measures taken both by China and by countries with frequent interaction with China to restrict contact with problem areas. In the US stock market companies with heavy China exposure have taken a greater hit to their shares than others – rationally so – but overall the trend has fallen well short of panic mode.

This could all change, of course, should new information surface that suggests a bigger and more complex problem. But in the absence of such information, it is at least somewhat heartening to see that all the trader-bots that make up daily trading volume were not programmed for hair-trigger freak-outs at the first sign of trouble. Maybe, hopefully, that’s progress.