MV Weekly Market Flash: What’s...

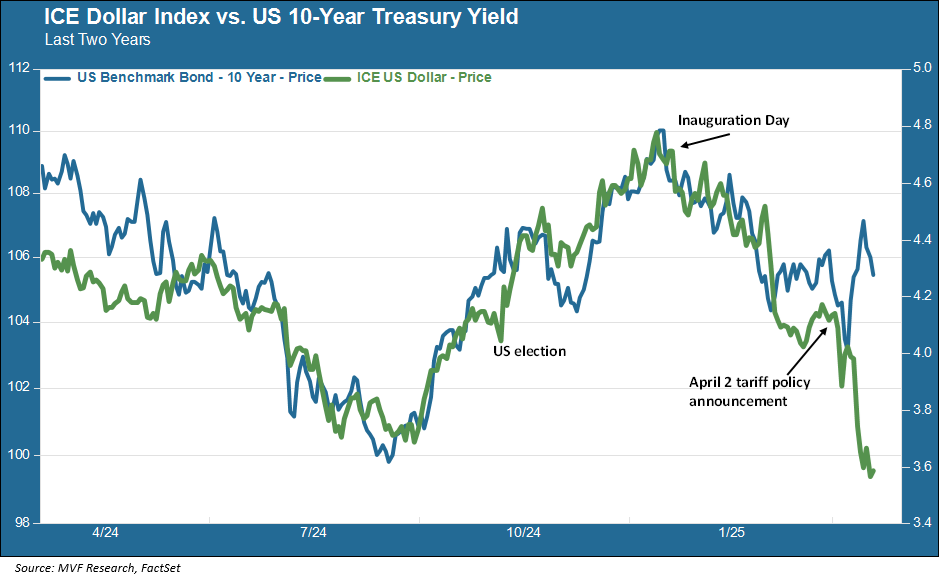

It’s a time-honored ritual in global financial markets: in times of trouble, seek out the safest of safe havens until the storm passes. Treasury securities and the US dollar fit that script – at least they have, prior to the current tempest. Amid the wild volatility on a near-daily basis in the stock market since the ill-fated tariff policy announcement in the White House’s Rose Garden on April 2, the US dollar has plummeted while yields on the safest (supposedly) bond instruments have soared. This sharp reversal from the way things usually work has a number of observers wondering about the long-term fate of the dollar.

The Legacy of 1971

The last time there was a discernible transition from one financial era to another was nearly 54 years ago. On August 15, 1971, then-President Nixon removed the gold exchange standard that pegged the US dollar to $35 per ounce of gold, the exchange rate framework set at the Bretton Woods conference in New Hampshire near the end of the Second World War. Gone for good was the relationship between gold and national currencies that had prevailed for most of the time since the advent of the Industrial Revolution.

Nixon’s closing of the gold window – the “Nixon Shock” in the parlance of the day – had many observers convinced that the days of dollar supremacy were over. The early 1970s was a period in which the hitherto uncontested economic leadership of the United States was challenged, particularly by the rapid rise of Japan and West Germany as viable competitors on the world stage. Inflation had started to tick up in the US by the late 1960s, and a recession in 1970 presaged an even deeper downturn in 1973. Eventually, the 1970s would earn its place in economic history as the decade of stagflation, where anemic growth and persistently high inflation conspired to make life miserable for average households trying to make ends meet and for central bankers trying to implement an effective monetary policy.

The dollar did fluctuate wildly over the course of this decade. But it remained the linchpin of foreign trade, the preferred asset for central banks’ stores of foreign exchange reserves, and the most sought-after currency for black market traders on the streets of Buenos Aires, Jakarta and other emerging markets in their earliest stages of growth. The dollar’s role as the world’s reserve currency was solidified as the 1970s gave way to the Global Age, when finance became the world’s most important industry and US financial institutions bestrode the globe with their dealmaking knowhow and endless pipeline of capital markets innovations. The US trade deficit grew over this time, but a ready supply of foreigners willing to hold US dollar-denominated assets to fund the deficits minimized the potential economic pain.

A Quandary for the Fed

By our reckoning, the Global Age ended for all intents and purposes with the global financial crisis of 2008. That crisis hit the US harder than many other countries, and the dollar index hit its lowest point since the Nixon Shock during the crisis. But the dollar soon regained its footing, losing nothing of its importance to the world economy, as the post-2008 environment came to be dominated by the Federal Reserve. The US central bank was arguably the most important economic entity of the 2010s, with its program of quantitative easing alongside ZIRP – zero interest rate policy – shoring up financial markets and (again, arguably) keeping the economy from tipping back into recession. The Fed reprised its role as the sun around which all else revolves during the Covid pandemic, unleashing a flood of bond-buying at the peak of panic during March 2020 that in turn made the world safe for speculators in any imaginable form of asset, wisely or less so, throughout the pandemic period.

Jay Powell’s Fed broke decisively with this pattern in 2022, when the central bank responded to the highest inflation since the 1970s with a resolute policy of monetary tightening that took interest rates from zero to a high (for the Fed funds rate) of 5.5 percent in just two years. The Fed defied the ceaseless expectations of the bond market that it would throw in the towel and pause or cut rates every time something went sideways somewhere in financial markets. Bringing inflation back down to two percent was, and remains, the central bank’s number one priority.

Which brings us to the difficult moment the Fed finds itself in today. Not only are there serious questions about what is going to happen to inflation given the ongoing chaotic quasi-implementation of tariffs by the administration, but there are even more fundamental questions about the ongoing role of the US dollar and, by extension, the traditional safe haven of the Treasury market. Last week, as we noted in our commentary last Friday, the Treasury market appeared close to having another March 2020 moment before the administration blinked and “paused” most of the April 2 tariffs.

Conditions since then have been somewhat more stable for stocks, bonds and currencies, but volatility and the potential for disruption hang over edgy market sentiment. Will the Fed have to intervene again to facilitate liquidity if the Treasury market goes pear-shaped again? What should the Fed’s policy be (if any) vis a vis a possible dollar retreat from its centrality as the world’s reserve currency? These are questions without clear answers. Sadly the Fed’s independence, which should not be an issue for discussion, is also in the mix. While we do not see a worst-case scenario here as a high probability outcome (that would be a nightmare for market sentiment), we can’t ignore it entirely. Strange times, these.