MV Weekly Market Flash: Will...

The equity market bulls had been running for more than five years. Over this time interest rates had come down dramatically, inflation was muted and most every fiscal quarter delivered a reasonably predictable uptick in real GDP growth. Markets had weathered a spate of political and financial scandals, as well as occasionally unnerving geopolitical flashpoints. All in all, there seemed to be no particular reason to complain or worry as summer transitioned to fall. Yet investors were edgy. A certain element of caution held in check what should have been giddy times on Wall Street, as if traders and investment bankers, contemplating their seven and eight figure bonuses, couldn’t shake the feeling that it was all a bit unreal. It’s quiet in here, said the young MBAs at Morgan and Salomon to each other as they stared at the monochrome numbers flashing silently on their Quotrons. It’s too quiet.

The previous paragraph could easily be imagined as some future market historian recalling the strange bull market of 2017 – up to the last sentence, anyway. Salomon Brothers is long deceased, and the cathode ray tubes of yesteryear’s Quotrons lie dormant in landfills, patiently awaiting the archaeologists of future millennia. No, the year in question is 1987. On October 19 of that year, a sudden flash of lightning made a direct hit on US equity markets. Major market indexes fell more than 20 percent in one day – the technical definition of a bear market. On October 20, market pros stumbled around the canyons of lower Manhattan asking: What happened?

Thirty years on, another generation of markets pros — contemplating another secular bull amid low interest rates, steady economic growth and uncomfortably subdued volatility – asks a different question: could it happen again?

A Bear By Any Other Name

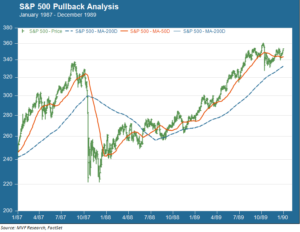

The chart below provides a quick snapshot of the Black Monday carnage – and the quick recovery thereafter.

That vertigo-inducing plunge on October 19 put the stock market squarely in bear territory, after a bull run that began in August 1982. But look how quickly the market recovered. By July of 1989 the S&P 500 had regained its pre-crash high. This new bull would go on running for more than a decade, ending only with the bursting of the tech bubble in 2000. For this reason, even though the 1987 market crash was technically a bear market event, we describe it in conversations with clients more as a disruption in the Great Growth Market that ran for 18 years (from 1982 to 2000). We think it is important to make this distinction. Secular bear markets, like the 14 years between 1968 and 1982, call for specific portfolio strategies. But there is very little that one can do about a sudden pullback like Black Monday. To respond to that question we identified above – could a 1987-style event happen again? – our answer is yes. Most certainly it could, and in the next couple paragraphs we will share our thoughts as to why. But a pullback based on some one-off exogenous risk factors – however steep – is not the same thing as a true bear market.

Portfolio Insurance: “Algo” Trading’s Beta Version

So what caused Black Monday? It took quite a while for the market experts of the day to put the pieces of the puzzle together, but in the end they identified the culprit: portfolio insurance. This seemingly benign term encapsulated an approach to institutional portfolio management that involved computer-driven signals to act as warning bells when market conditions appeared risky. Sound familiar? It should, because the crude hedging strategies that made up portfolio insurance circa 1987 were the ancestors of today’s ultra-sophisticated quantitative strategies known by those in the game as “algo” (for “algorithm”) trading.

If you look at the chart above you will see that, a few days before Black Monday, the stock market moved meaningfully lower after soaring to new record highs. For a combination of reasons involving the rate of change in the market’s advances and declines, underlying volatility and a few other factors, the portfolio insurance triggers kicked in and began selling off positions to build hedges. On October 16, the Friday before the crash, the S&P 500 pulled back more than 5 percent as the hedging begat more hedging. On Monday morning the sell orders cascaded in, but there were no buyers. That’s what brought about the carnage.

Peaks and Troughs

Given how much money is currently invested in the offspring of portfolio insurance, the really interesting question is not “could it happen again?” but rather “why hasn’t it happened more often?” For one thing, the ’87 crash did bring about some institutional reforms – operational circuit-breakers and the like – to try and minimize the damage a tidal wave of one-directional orders could bring about. These safeguards have worked on a number of occasions.

For another, the vast diversity of quantitative strategies itself is a kind of check and balance. Every algo program has its own set of triggers: buy when the German Bund does X, sell when Janet Yellen says Y, write a bunch of straddles when China’s monthly FX reserve outflows top $100 million. Put all these out there in the capital markets and they act sort of like the ocean when the peak of one wave collides into the trough of another – they cancel each other out. But that is reassuring only up to a point. It is not hard to imagine that a perfect storm of signals could converge and send all the algo triggers moving in the same direction – everyone wants to sell, no one wants to buy. Crash!

Lessons from the Crash

So, if such a perfect storm were to happen and blindside portfolios with massive short term losses, are there lessons to be learned from 1987? Quite so. It should be clear from the above chart that the worst thing an investor could have done on October 20, 1987 would have been to sell in a panic. In fact, those of us who have been at this long enough to remember the day (and do we ever!) recall that Wall Street’s trading rooms were never more frenzied with buy orders than in the weeks after Black Monday. Portfolio managers may not have yet known exactly why the crash happened – but they knew that the macroeconomic context hadn’t changed, that there were no new geopolitical crises, and that stocks with stratospheric P/E ratios after a long bull run were suddenly super-cheap. That, largely, is what explains the quick recovery, explains why 1987 was not a “real” bear market and explains why, all else remaining more or less unchanged, the prudent response to an out-of-the-blue event is to stay disciplined.