MV Weekly Market Flash: The Jobs Market Is Not OK

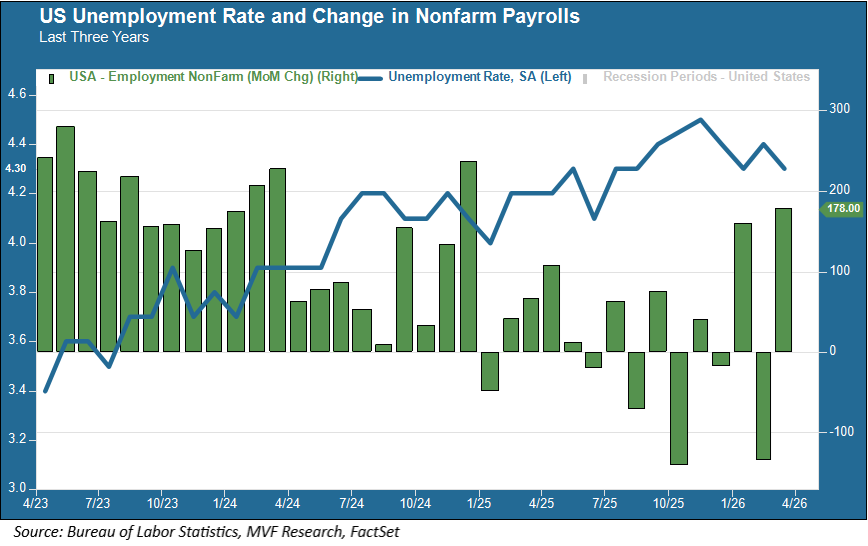

Read More From MVThe monthly jobs report from the Bureau of Labor Statistics will come out in two weeks from today. Do you want to hazard a guess as to the number of nonfarm payroll (NFP) gains reported for the month of April? Good luck with that – see below. In the past fifteen months we have had nine months of payroll gains and six months of payroll losses, according to the BLS data. And this chart doesn’t reflect an even more bizarre facet of the BLS report, in which initial estimates are subject to sweeping revisions. Case in point: the initial report...

Read MoreMV Weekly Market Flash: The Alfred E Neuman Market Returns

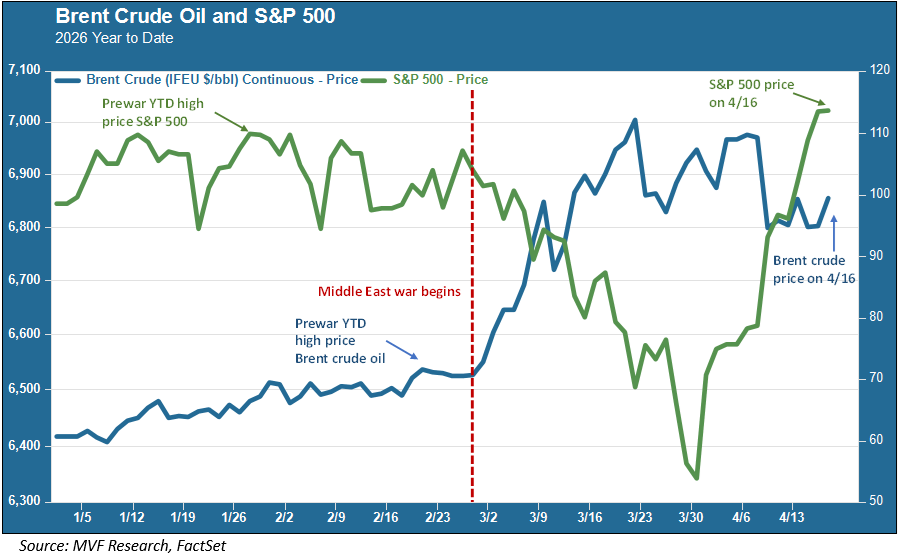

Read More From MVOn Wednesday this week the S&P 500 stock index closed above 7,000 for the first time ever, and thus gave traders the thrill of two big things on the same day: a nice round number (oh, how we love crossing the round number thresholds), and a record close to boot! So the stock market has clawed back all its losses since the onset of the Middle East war, and then some. Is this the dawn of another one of those magic carpet rides the market takes us on from time to time, or is there potentially cause for a pause?...

Read MoreMV Weekly Market Flash: The Importance of the Up Days

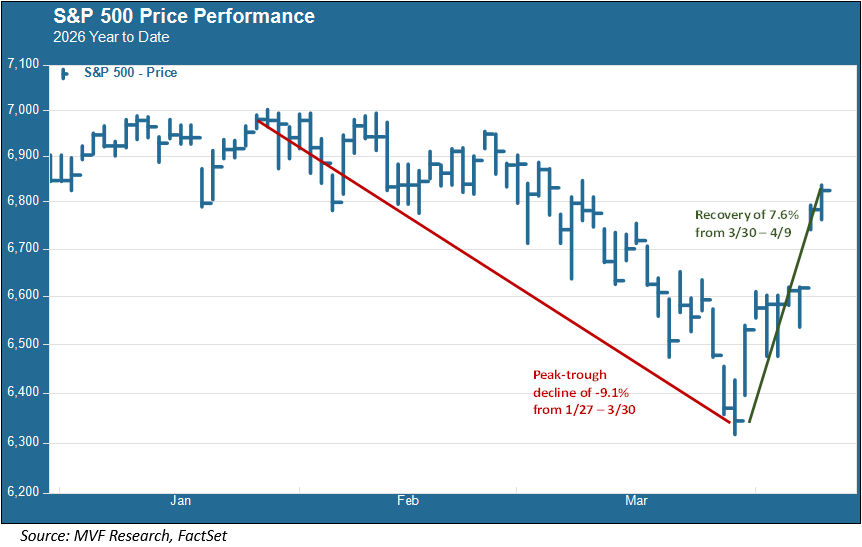

Read More From MVPatience and discipline. This is the mantra we have been encouraging our clients to embrace from day one. The past several weeks has constituted one of those times when following that mantra is exceptionally important. It is also exceptionally hard, because it requires control over our very powerful lizard brain impulses of fear and greed. An Anthology of Disruption Because it is hard to practice the art of patience and discipline when markets go pear-shaped, we pay very close attention to the facts around disruptive events. Specifically, we have documented every drawdown in the S&P 500 of five percent or...

Read MoreMV Weekly Market Flash: Hard Times in Private Credit

Read More From MVMarch was not a great month in most asset classes. The S&P 500 lost a bit more than five percent from the month’s opening bell to its closing coda a couple days ago. Many other equity benchmarks took it on the chin even harder. Bond yields rose, and oil prices rose by a whole lot more. But for all the short-term pain, at least investors in these highly liquid markets had ready access to their capital if need be. Not so for the multitudes, retail and institutional alike, who over the past several years heard the siren song of private...

Read MoreMV Weekly Market Flash: Let A Thousand Scenarios Bloom

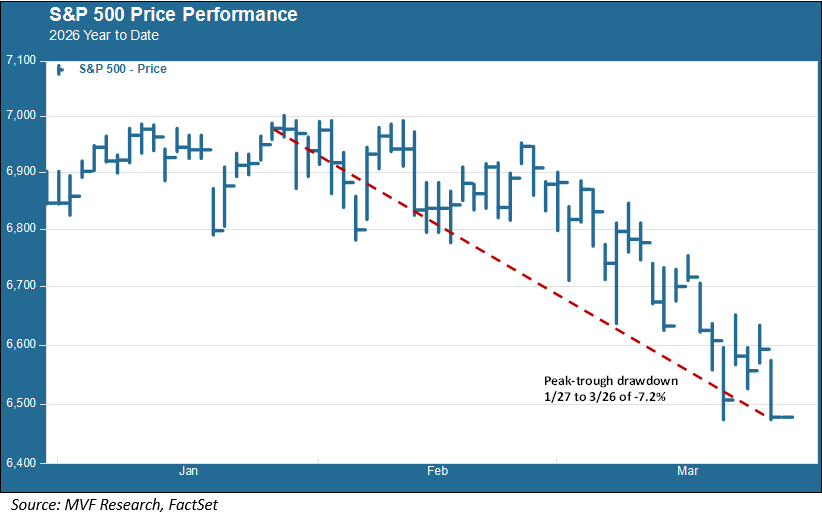

Read More From MVHow bad could it get? That is the question on the minds of many investors as the war in the Middle East slogs on with no apparent clarity about, well, anything. Let’s do a quick check-in to see where we are as of this somewhat rainy Friday morning in the Washington, DC environs where we ply our trade. When In Doubt, Equivocate The S&P 500 stock index has lost around 7.2 percent of its value from its last record high, on January 27, to its close on Thursday. That is considerable, but the index has yet to cross either of...

Read MoreMV Weekly Market Flash: Push and Pull in the Bond Market

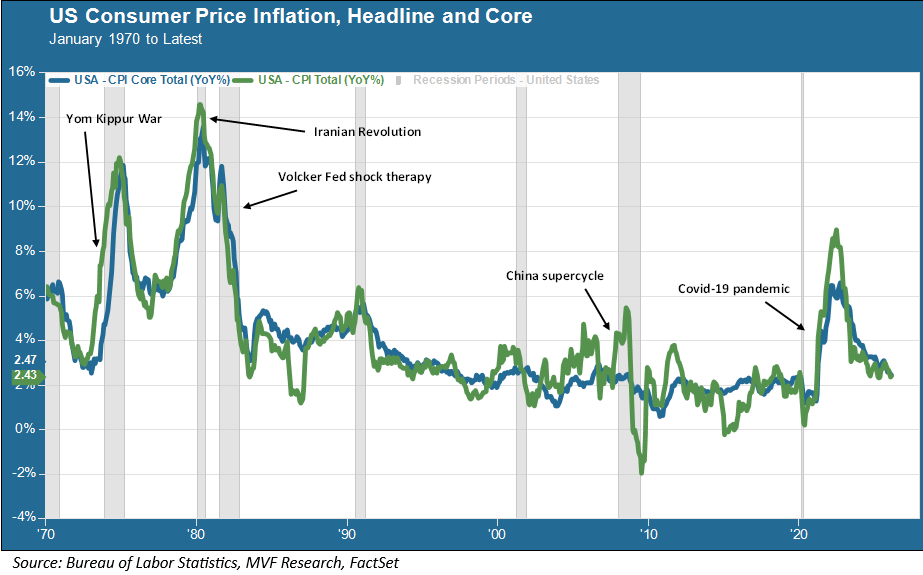

Read More From MVThis is not stagflation! Or so Jay Powell insisted, during the Wednesday press conference this week following the Federal Open Market Committee meeting that, as widely expected, kept US policy rates on hold at present levels. Stagflation was a thing we had to deal with, very harshly, in 1979, when turmoil in Iran was just one of many factors fanning the flames of consumer inflation. Paul Volcker’s Fed had to raise the Fed funds rate, ultimately to as high as 20 percent, to corral inflation and reinvigorate the economy’s potential to grow. Anything less than the experience of 1979-80, in...

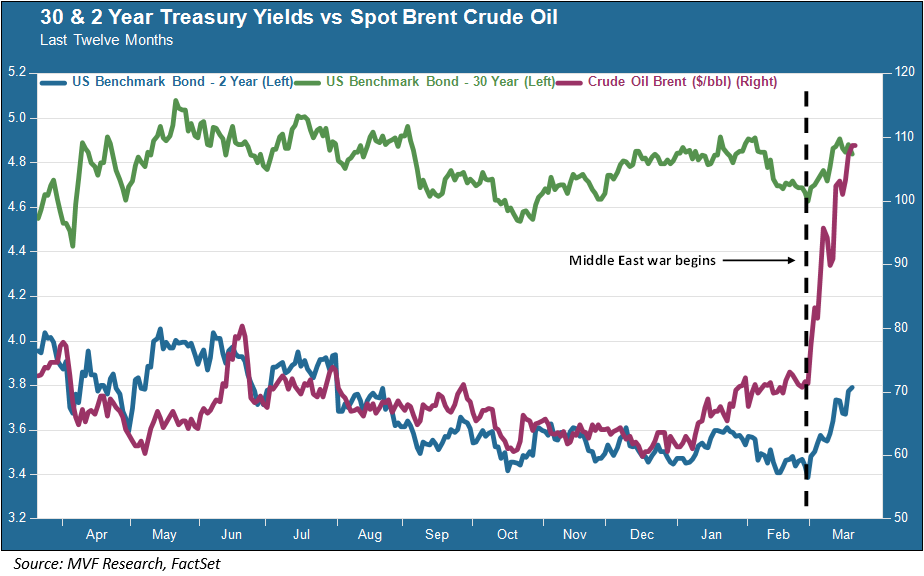

Read MoreMV Weekly Market Flash: The Least Useful CPI Report Ever

Read More From MVOn Wednesday this week the Bureau of Labor Statistics released the Consumer Price Index report for February. Economists had been expecting to see a year-on-year increase of around 2.4 percent in the headline inflation number, with an attendant gain of 2.5 percent in core CPI, excluding the volatile categories of energy and food. That is more or less what happened. But it happened last month; in other words, before a series of air strikes by the US and Israel had the effect of shutting down the passage of shipping traffic through the Strait of Hormuz. As a refresher from last...

Read MoreMV Weekly Market Flash: The Menace of Stagflation

Read More From MVExactly one week ago, the Bureau of Labor Statistics published its January report for wholesale prices, showing a 3.6 percent year-on-year rise in the Producer Price Index, much larger than economists had expected. Today, the same Bureau of Labor Statistics issued its monthly jobs report noting, rather coyly, that nonfarm payrolls had “edged down” by 92,000 in February. Now, perhaps whoever edits the BLS report wanted to soften the delivery of bad news for whatever delicate sensibilities might be perusing the jobs numbers, but a decline of 92,000, when economists had been expecting a gain of 60,000, is not “edging...

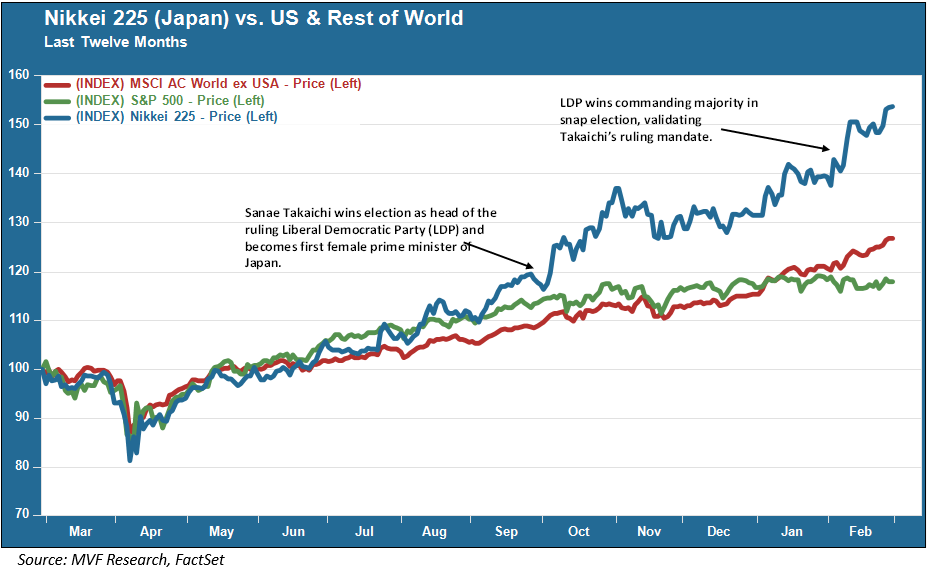

Read MoreMV Weekly Market Flash: Japan Rises, Again

Read More From MVWhen Commodore Matthew Perry sailed into what is now Tokyo Bay in July 1853, the Industrial Revolution had already been galvanizing Western economies for a half century. Japan, by contrast, was an isolated feudal backwater, intentionally cut off from the rest of the world since the beginning of the Tokugawa Shogunate in 1603. Faced with the obvious technical superiority of the West as they stared down the cannon barrels of Perry’s Black Ships, Japan’s leaders realized that nothing short of a far-reaching transformation away from the ossified practices of the ruling samurai class was going to be required. Via the...

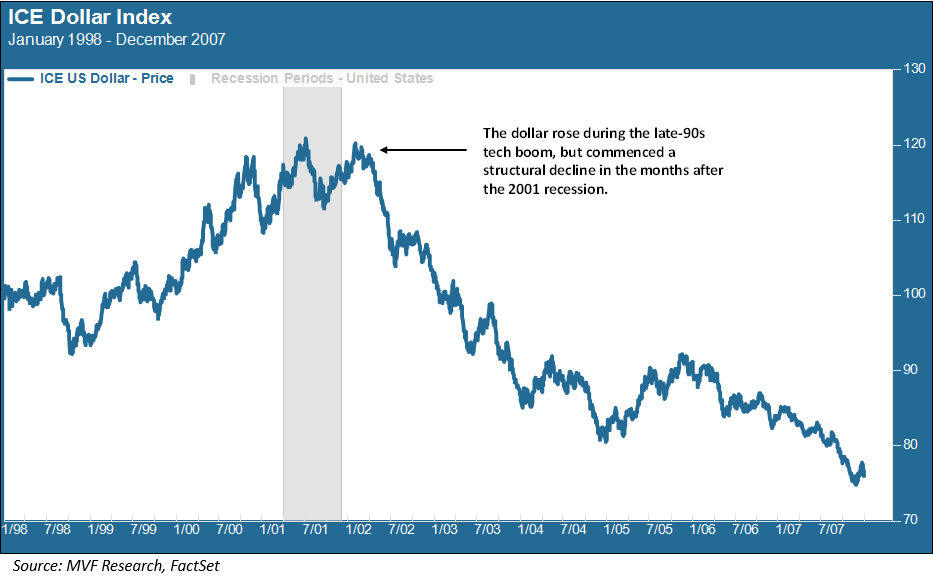

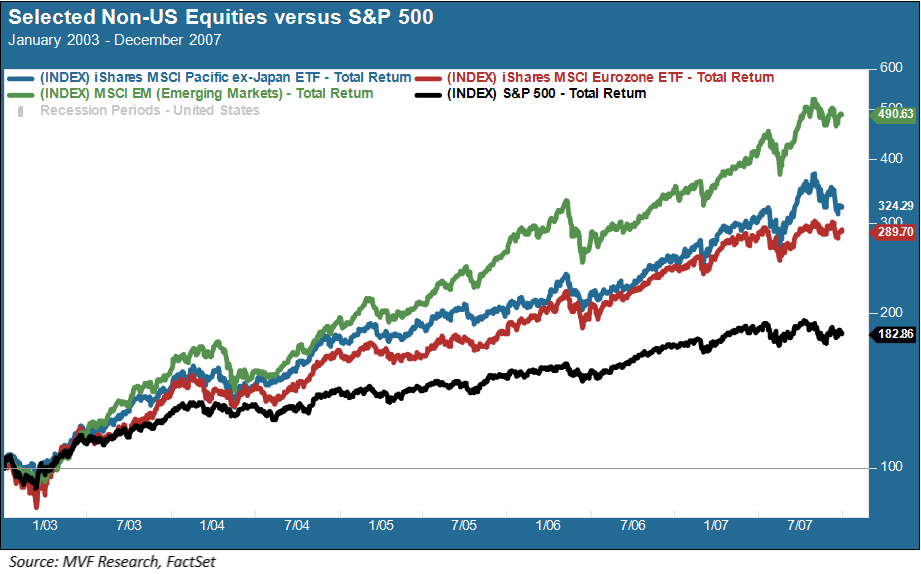

Read MoreMV Weekly Market Flash: The Last Time Non-US Ruled the Roost

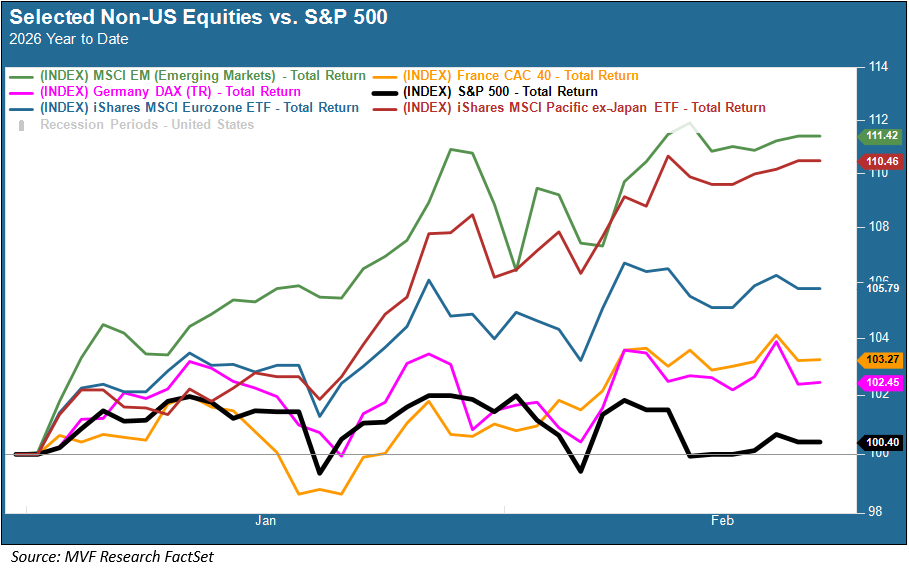

Read More From MVThe rotation out of US equities is into its second year and going strong. The rest of the world may be having its share of problems, but underperforming stocks is not one of them. Here is a brief snapshot of how things are going in other parts of the globe, relative to the flattish ways of the S&P 500 thus far. This got us to thinking about the last time non-US equities gripped the imagination and enthusiasm of the investing crowd. Let’s take a little trip back to the quaint world of this century’s first decade. Swan Song for the...

Read More